Development charges, which are paid to enhance or intensify the use of

some sites, are headed north for residential use at the upcoming DC rate

revision effective March 1, say property consultants.

They cite the increase in private home values since last year as well as

aggressive land bids for residential sites at state tenders in the past six

months.

On average, DC rates for landed and non-landed residential use could rise

about 5 to 10 per cent. However, consultants are predicting that rates for

commercial, industrial and hotel use could remain flat.

The upcoming DC rate revision will also be monitored by those trying to

embark on collective sales, especially for sites whose redevelopment would

involve sizeable DC payment. DC is part of total land cost to a developer.

If the DC rate increases significantly and the value of the site remains

constant, the developer will offer owners less for the site, explains CB

Richard Ellis executive director Jeremy Lake.

‘The problem today is that there’s already a price gap between

owners’ and developers’ expectations. This will be compounded if

there’s a significant hike in DC rates, in the case of sites with a

significant DC component. The current environment (of rising private

residential price expectations) is not conducive to owners reducing asking

prices,’ he adds.

‘Hence for en bloc sites with significant DC component, the exposure to

DC volatility can be very unhelpful in a rising market, whereas sites with

zero or low DC component are fairly immune to DC volatility and those are

good sites to work on.’ Mr Lake reckons that the next DC rate revision on

Sept 1 may be more keenly watched – than the March 1 update – as a

higher number of en bloc sale efforts are likely to be at a more advanced

stage then.

DC rates – which are revised on March 1 and Sept 1 each year – are

specified by use groups (such as landed and non-landed residential,

commercial and hotels) across 118 geographical sectors throughout Singapore.

The review is conducted by the Ministry of National Development in

consultation with Chief Valuer, who takes into account current market

values.

Colliers International is projecting 8 to 10 per cent rise in average DC

rates for non-landed residential use from March 1. The biggest hikes of up

to 20 per cent are likely to be in places like Serangoon Avenue 3, Upper

Thomson Road and Sengkang West Avenue where winning land bids at state

tenders have been at substantial premiums of 48-86 per cent to land values

imputed from the Sept 1, 2009 DC rates for these geographical sectors, says

the firm’s director Tay Huey Ying.

Suburban locations could see a bigger rise in DC rates than upmarket

locations as last year’s rebound in home sales and prices was led by the

mass market segment, she argues.

Private-sector land deals too point to higher DC rates. For instance, the

Parisian site at Angullia Park was sold in October at $2,058 psf per plot

ratio – about 70 per cent above the DC-rate implied land value for the

area.

DTZ’s SE Asia research head Chua Chor Hoon reckons that non-landed DC

rates will go up 15 to 25 per cent from March 1. Jones Lang LaSalle’s

associate director (research and consultancy) Desmond Sim predicts 10-15 per

cent hikes in non-landed residential DC rates in mass-market suburban

locations, outpacing a 5-8 per cent rise in prime districts.

As for landed residential DC rates, he forecasts a 10-15 per cent

increase across all geographical sectors, with a bigger increase likely for

Sentosa Cove and Good Class Bungalow Areas.

CB Richard Ellis executive director Li Hiaw Ho notes that the official

price indices for detached, semi-detached and terrace houses rose 20-odd per

cent from July to December 2009. In addition, 2009 saw the highest total

value of GCB sales at $1.64 billion. He forecasts an average 5-10 per cent

rise this round for landed rates.

Mr Li forecasts DC rates for commercial and industrial use will remain

unchanged or even fall very marginally.

Colliers’s Ms Tay, who is projecting an up to 5 per cent climb in

average DC rate for industrial use, says: ‘The government is unlikely to

make significant upward adjustments to DC rates for industrial use group in

general in the upcoming review given the nascent recovery of the

manufacturing sector and the industrial property market. Also, JTC Corp

industrial land rents have not been adjusted since they were revised

downward in January 2009, says Ms Tay.

She reckons commercial DC rates will remain largely unchanged as office

rents have remained weak.

2010 February 24 BUSINESS TIMES

Sentosa has seen a big jump in

development charge (DC) rates, reflecting higher land values on the island

following this month's opening of Resorts World Sentosa (RWS).

On average, the government is raising DC

rates (payable for intensifying or enhancing the use of some sites) about 12

per cent for landed residential use from March 1; but in Sentosa, they will

climb 17.3 per cent. For non-landed residential use, Sentosa saw a 10 per

cent hike in DC rates compared to the average rise of about 8 per cent. And

while DC rates for commercial use will be cut roughly 2 per cent on average

against the backdrop of weak office rentals, Sentosa is the only location

where they will be raised - to the tune of 12.5 per cent.

It is also the only location where the

government increased the hotel-use DC rate; the hike was 12.2 per cent. In

all other locations, the DC rate for hotel use (which also covers hospitals)

was left untouched.

DC rates - which are revised on March 1

and Sept 1 each year - are specified by use groups across 118 geographical

sectors throughout Singapore. The review is conducted by the Ministry of

National Development in consultation with the Chief Valuer, who takes into

account current market values.

Some analysts pointed to an interesting

trend emerging in the Central Business District. DC rates for commercial use

in the CBD fell further while non-landed residential rates rose and actually

surpassed the commercial rates. This could mean paying a higher DC for those

who redevelop old CBD office blocks into apartments and could impact such

conversions, especially in the case of 99- year leasehold sites as their

owners would also want a lease top- up, says DTZ's South- east Asia research

head Chua Chor Hoon.

Jones Lang LaSalle's SE Asia research

head Chua Yang Liang goes a step further, predicting that the new trend

could have an 'unexpected effect of encouraging the redevelopment of

existing older office stock into the same office use and discouraging

conversions to residential'. Jones Lang LaSalle's (JLL) analysis showed that

DC rates for non-landed residential use were raised for 116 geographical

sectors and left unchanged for the remaining two areas.

The biggest hike of 15.4 per cent was

seen in three sectors: 91 (which covers the Mountbatten, Meyer and Broadrick

areas); 98 (Tampines, Bedok Reservoir, Bedok North, Kembangan); and 101 (Paya

Lebar Way/Eunos/Sims Avenue).

This was followed by Sector 76 (Everton/Spottiswoode

Park) with a 14.5 per cent increase. Market watchers attribute this to last

October's en bloc sale of Dragon Mansion at a land price about 68 per cent

above the land value implied by the prevailing Sept 1, 2009 DC rate for the

location.

Also, the geographical sectors covering

Serangoon Ave 3, Upper Thomson Rd and Sengkang West Avenue - where

residential sites have been sold at bullish prices at state tenders in the

past six months - were raised 12.5 per cent, 10.5 per cent and 9.1 per cent

respectively.

Colliers International executive director

(investment sales) Ho Eng Joo said that overall, the growth in non-landed

residential DC rates may hamper developers' landbanking plans, especially

for collective sales sites that require DC payment.

Credo Real Estate managing director

Karamjit Singh, however, said yesterday: 'Three quarters of the en bloc

projects our company is working on don't involve any DC payment. As for the

rest, DC as a component of the entire land cost is not very high and hence

the increase in DC rates will have minimal impact on the en bloc sale

exercise.'

For landed residential use too, charges

were raised in 116 sectors and left unchanged in the other two.

Besides Sentosa, other areas with the

biggest hikes include Holland/Dunearn Rd/Sixth Avenue (up 17.1 per cent) as

well as the Good Class Bungalow areas of Botanic Gardens/Gallop Rd/Tyersall

and Ridout/Peirce Hill/Swettenham Road (each up 16.9 per cent), JLL's

analysis shows.

Commercial DC rates were trimmed between

3.2 and 13.3 per cent in 23 sectors. The biggest chop was in the Cecil

St/Robinson Road area. There were also cuts in other parts of the financial

district, such as Marina Bay, Raffles Place and Fullerton Road, as well as

in the Thomson/Moulmein, Newton Circus, Bugis and Tanglin/Cuscaden areas.

- 2010 February 27 BUSINESS

TIMES

Enbloc sales modified

A new amendment bill introduced in

Parliament yesterday will make it harder for property owners to keep

re-trying for a collective sale.

But analysts said other changes - such as

allowing contested sales to bypass Strata Titles Board (STB) hearings and

reducing the number of extraordinary general meetings (EGMs) that must be

held - could help to speed up the en bloc sale process.

A key revision that has been tabled will

make it harder for motivated owners to re-start an en bloc process once it

fails as there will be a two-year restriction period.

Within this restriction period, the first

re-try to convene an EGM will need 50 per cent of share value or number of

owners. And for the second and subsequent re-tries, 80 per cent will be

needed.

Right now, the support of either 20 per

cent of owners by share value or 25 per cent of the total number of owners

is needed to call an EGM to start the process.

'The objective of this change is to

discourage numerous attempts at en bloc sales where there is insufficient

level of interest and support from owners,' said the Ministry of Law in a

statement. It also added that this move prevents management committee funds

from depleting.

The amendment bill to the Land Titles

(Strata) Act also looks to streamline the role of the STB and balance the

interests of minority and majority owners. The changes are expected to take

effect in June.

'In recent years, a number of en bloc

sale applications have become highly contentious, with objectors raising

questions on points of law ranging from fiduciary to constitutional law,'

said the Ministry of Law. 'Many of these cases have ended up in the High

Court and even the Court of Appeal. This has resulted in lengthy and costly

proceedings.'

In addition, once a sales committee (SC)

is formed it will have one year to obtain the first signature for the

collective sale agreement (CSA) or it will be automatically dissolved. This

is to ensure that the sales process is not dragged out.

Analysts were not too worried about the

two-year restriction period.

Credo Real Estate managing director

Karamjit Singh said en bloc transaction volumes are driven more by market

forces and owners' expected gains.

'But having said that, the two-year

restriction period following a failed attempt may be disadvantageous to some

projects that may want to capitalise on improved market sentiments, should

that happen after the failed attempt,' said Mr Singh.

But Chua Chor Hoon, head of DTZ's

South-east Asia research team, said that the two-year restriction period

could have a large impact as the definition of a failed attempt covers a

whole host of situations - including right at the beginning, when the quorum

required for an EGM to discuss a collective sale is not met within an hour

and the EGM is dissolved.

The new amendments could also speed up

the process 'in theory'.

'It helps to eliminate some of the

ambiguities in the current legislation and will help to expedite the

process,' said Ho Eng Joo, executive director for investment sales at

Colliers International.

The Ministry of Law last amended the Act

in 2007, introducing changes to make the en bloc sale process more

transparent.

Then, it was decided that SCs will have

to be properly formed and elected. It was also decided that CSAs will have

to be witnessed by lawyers who can clarify doubts and explain terms and

liabilities. And even after they signed, potential sellers were given a

five-day 'cooling-off period' during which they can change their minds.

This latest round of changes comes as

activity in the collective sales market appears to be picking up after

falling off sharply in 2008 and 2009.

According to data from CBRE Research,

there were 110 collective sale transactions worth a total of $11.9 billion

in 2007. This fell to eight deals worth $381 million in 2008 and just one

deal worth $101 million in 2009 as the property market took a downturn.

But since the start of this year, five

collective sales worth $275 million in all have gone through - signalling

that the en bloc market could be picking up again.

'There has been more interest on the

ground from Q3 and Q4 last year,' said Jeremy Lake, executive director of

investment properties at CBRE.

Most analysts were also disappointed that

two measures, in particular, were not axed.

'I am disappointed that they have not

removed the cooling off period of five working days, notwithstanding the

requirement that a solicitor must witness the signatures of the owners

executing in Singapore,' said law firm Rodyk & Davidson partner Norman

Ho. CBRE's Mr Lake likewise pointed out that the requirement for the CSA to

be witnessed by lawyers is the 'biggest hindrance' to a collective sale

going through.

'The main problem that SCs face at the

moment is securing the 80 per cent or 90 per cent agreement needed and that

is principally due to the need to have the signing witnessed by lawyers,' he

said. Sometimes it was difficult to get a lawyer and owner together at the

same time to get the CSA signed, he said.

- 2010 April 27 BUSINESS

TIMES

While the market mulls over the impact

that rule changes will have on collective sales, the spotlight has fallen on

developers sitting on prime sites acquired during the previous en bloc boom

in 2006-2007.

|

| Hot asset: Developers

of prime sites like Farrer Court (above) will time their project

launches more carefully |

If the proposed changes make it tougher

for prime freehold residential sites to make their way to the market, that

will be good news to developers who are already holding such sites acquired

earlier.

A compilation by property consultant CB

Richard Ellis shows that developers currently have 26 sites in prime

districts 9, 10 and 11 snapped up in collective sales in 2006 and 2007 where

new projects are still to be launched.

These sites are planned for redevelopment

into nearly 4,300 new homes. Outside the prime districts, developers could

build a further 4,700 homes on 16 sites purchased through collective sales

in 2006-2007

CapitaLand, City Developments Ltd (CDL),

Wing Tai, GuocoLand and Overseas Union Enterprise are among the developers

who bought prime district en bloc sale plots earlier. For instance,

CapitaLand, together with its partners, acquired the Farrer Court plot and

is planning a 1,715-unit redevelopment project. Hong Leong Group (including

CDL) has exposure to six sites slated for development into over 600 units in

locations like Leonie Hill, Anderson and Thomson roads.

These sites and projects will become more

precious to developers and they will want to time their launch more

judiciously if it gets tougher to replenish landbank in this segment through

en bloc sales, say industry observers.

CB Richard Ellis executive director

Jeremy Lake says: 'The proposed amendments are unlikely to facilitate the en

bloc process significantly and as such, the number of collective sales

coming to the market is likely to remain relatively limited.

'From a developer's point of view, it

will be more difficult to replace landbank in prime areas so those who have

such sites may think more carefully about the timing of launch of new

projects on these sites as it will not be easy to find replacement land.'

Giving a more pessimistic take, a

developer said: 'I don't think anyone would be too far wrong to say that en

bloc sales are just about the only source of supply for prime district

freehold sites. The proposed amendments to the Land Titles (Strata) Act will

put the 'last nail in the coffin' for en bloc sales in the near future, and

the market will be completely dried up for freehold District 9, 10, 11 land

supply.'

This will create upward pressure on land

prices, he added.

Putting things in perspective, DTZ senior

director (investment sales) Shaun Poh says: 'En bloc sales in many

developments have already been activated and these are unlikely to be

affected by the proposed amendments. The supply from this source should be

enough for the market for the time being.

'However, the future pipeline of en bloc

sales will be affected.'

On Monday, the Ministry of Law released

proposed amendments that will among other things make it harder to restart a

collective sale within two years of a failed attempt. Any attempts to

convene EGMs to appoint a sales committee during this period will require

higher requisition levels from owners - 50 per cent by share value or total

number of owners for the first re-try and 80 per cent for any subsequent

attempts.

'Already it's not easy to secure

requisitions for EGMs based on existing thresholds of 20 per cent by share

value or 25 per cent of number of owners,' says DTZ's Mr Poh.

'Now that they're proposing to raise the

threshold for restarting previously failed en bloc attempts, it's going to

be more difficult for those who want to have another shot when, say, the

market suddenly turns hot.'

On a more positive note, Credo Real

Estate managing director Karamjit Singh notes that the instances of failed

attempts that will be affected by the two-year restriction do not cover

cases where owners' 80 or 90 per cent majority consent was secured but the

Collective Sales Agreement (CSA) expired because a buyer could not be found

in time.

'The projects that may be affected are

likely to be those that had attempted an en bloc sale when they should not

have, either owing to the project not being fundamentally 'enblocable' or

the market was not on their side to an extent that the majority owners

rejected the proposal,' he said.

MinLaw hopes its proposal will discourage

repeated attempts at en bloc sales where there isn't enough support from

owners.

Industry players lauded MinLaw's proposal

to streamline the number of EGMs, which should speed up the process. 'We

expect to see further en-bloc activity this year,' said Chris Fossick,

managing director Singapore and South East Asia for Jones Lang LaSalle.

Others, however, complain that the the

ministry is not doing anything to mitigate bottlenecks caused by the need to

have lawyers witness signing of the CSA.

This has also jacked up legal costs. Some

have suggested doing away with this requirement since those who sign are

given a five-day cooling-off period. - 2010

April 29

BUSINESS TIMES

Property Groups find Asset-Divestiture

trying

of aborted divestments by Singapore

property groups lately highlights the challenges of relying on asset sales

in the current environment.

Last weekend's edition of BT featured two

stories on the same page, on Singapore's two biggest listed property groups

- CapitaLand and City Developments Ltd (CDL). Both are in the same boat,

with their respective planned divestments of overseas assets not completed.

CDL's London-listed hotel subsidiary

Millennium & Copthorne Hotels announced that the agreement for the

disposal of Millennium Seoul Hilton hotel to Korean group Kangho AMC Co had

been terminated as the buyer was unable to finalise its financing

arrangements amid the global financial turmoil.

CapitaLand's 30 per cent-owned associate

Inverfin Sdn Bhd, which owns Menara Citibank tower in KL, reported that the

sale-and-purchase agreement for the sale of the office tower had been

terminated as the buyer, IOI Corporation Bhd, did not pay the balance

purchase price on the completion date.

There have also been instances of

transactions of Singapore buildings not being completed. Ho Bee announced

last month that its proposed $30 million sale of Frontech Centre, an

industrial building in Bukit Merah, had fallen through. The buyer is

understood to have been US fund group Angelo Gordon. BT also reported last

month that Australian property fund manager Blaxland did not go ahead with

completing its planned acquisitions of eSys Technologies' building in Changi

North and SH Cogent Logistics' warehouse building in Penjuru Close in Jurong.

The pullouts reflect the difficult

conditions for property investment sales, caused by several factors.

Firstly, funding is tight. But even potential buyers with financial muscle

may get cold feet or decide it simply makes more sense to walk away from

their purchase now and forfeit the deposit, as sliding property values will

present more attractive investment propositions in due time. There may also

be other issues at play, such as exchange rate fluctuations. For instance,

from a potential buyer's perspective, the Aussie dollar's 21 per cent

depreciation against the Singapore dollar in the past three months would

make purchasing Singapore properties less attractive.

Putting things in perspective, a seasoned

property consultant said: 'The current climate makes asset sales difficult,

whether you're selling an apartment or a shopping centre.'

Property groups will have difficulty

selling assets even to their sponsored real estate investment trusts (Reits).

With the stockmarket slide, Reits are trading at very high yields, which

makes it difficult for them to make yield-accretive acquisitions. And the

current tight funding environment affects Reits as well; their priority

these days is refinancing existing debt instead of sourcing new debt for

further acquisitions.

The situation is likely to continue for

at least the new few quarters; that will have implications for Singapore's

property groups. Heavyweight CapitaLand has booked handsome profits from

divesting assets in the past few years. In the past two years, the group has

divested some $9 billion of assets - an exercise that has generated well

over $1 billion in profits.

The group still has other assets that it

could potentially divest, such as its industrial property portfolio here and

even some of the office blocks held by its sponsored Reit CapitaCommercial

Trust.

Prior to the global financial crash,

CapitaLand would have had a high chance of success if it had continued on

its path of asset disposals. Now, buyers are scarce and even those that are

around would demand distressed sale prices (as cushion against further

declines in property values after their purchase).

The trying financial climate will affect

asset divestment strategies of even a heavyweight like CapitaLand. But at

least it has stronger financial muscle to weather this storm even if it

can't make major divestments in the near future.

Smaller players are not in the same boat.

Some companies burdened with heavy debt and which had been hoping to unload

some of their properties to improve their balance sheets will be caught if

they can't sell their assets.

Hopefully, the malaise in the property

investment sales market will not drag on too long.

- 2008 December 2 BUSINESS

TIMES

Property market now shows classic

signs of downturn

Analysis of Q3 caveats by DTZ points

to new trends relating to subsales, foreign buying, HDB upgraders

Three classic signs of a Singapore

property downturn have emerged in the third quarter - a slide in subsales

and foreign buying, but a bigger share of HDB upgraders in the private home

buying pie.

Property consultancy DTZ's analysis of

caveats for private home purchases shows that total subsales of non-landed

private homes fell 8 per cent to 473 units in Q3 from the previous quarter.

Subsales also accounted for a smaller 13 per cent share of purchases of

non-landed private homes in Q3, compared with 16 per cent in Q2.

Subsales of high-end condos/apartments

slowed down even more in Q3 2008. The number of subsale purchases involving

units priced at least $1,000 psf fell 24.2 per cent quarter-on-quarter to

only 213 transactions, accounting for 45 per cent of overall subsales of

non-landed private homes in Q3, against 54 per cent in Q2 2008.

The number of foreign buyers (including

permanent residents) of private homes (both landed and non-landed) slid 6

per cent quarter-on-quarter to 903 in Q3. Also, these buyers made up 22 per

cent of total private home deals in the quarter, down from 25 per cent in

Q2.

DTZ senior director (research) Chua Chor

Hoon said: 'A large proportion of foreigners buy for investment. Hence when

prices are falling, there is less interest. Furthermore, with economies and

property markets slowing down all over the world, many of the foreigners

have been affected back home and they may pull out their overseas

investments.'

DTZ executive director Ong Choon Fah also

points out that attractive property values are emerging in other cities

which Singapore will be competing with. 'Foreign investors

have lots more opportunities to

consider where to invest,' she added.

The dip in subsales may be due to the

fact that it has become more difficult for 'specuvestors' and speculators to

offload their properties in the current quiet market.

'For investors who take a long-term view,

especially for better assets, the tendency would be to ride out the market,'

says Mrs Ong.

HDB dwellers tend to make up a bigger

proportion of private home buyers during a property downturn. 'Many of them

are buying for owner occupation. Some may be sitting pretty on gains on

their existing HDB flats which they bought directly from the HDB some years

ago. Together with CPF savings, it may be easier for them to cross over to

private homes,' notes Mrs Ong.

Buyers with HDB addresses picked up 1,718

private homes in Q3, up 34 per cent from the previous quarter.

Their share of caveats lodged for private

home purchases rose to 41 per cent in Q3, from shares of 34 per cent in Q2

and 28 per cent in Q1 this year. HDB upgraders' 41 per cent share of private

home purchases in the July-Sept quarter was the highest quarterly share in

four years.

'The trend was supported by the narrowing

gap between HDB resale flat prices and private home prices in Q3, as HDB

resale prices continued to increase while private home prices fell,'

Ms Chua said the latest Q3 jump in

private homes bought by HDB dwellers was mainly in the primary market. The

number of units these HDB dwellers picked up from developers leapt 89 per

cent from Q2.

Livia in Pasir Ris and Clover by the Park

in Bishan were the two most popular projects among HDB buyers in Q3, with

192 units and 142 units respectively sold to HDB upgraders.

Analysts say HDB upgraders' share of

total private home purchases may rise further. In Q2 2002, their share

surged to 81 per cent and at the trough of the Asian Financial Crisis

property slump in Q4 1998, the figure was 68 per cent.

Subsales refer to secondary market deals

in projects that have yet to receive their Certificates of Statutory

Completion. This may be anywhere from three to 12 months after the project

gets its Temporary Occupation Permit (TOP).

DTZ said that for total subsale deals of

non-landed private homes, the median price continued to fall in Q3, easing

11 per cent quarter-on-quarter to $941 psf - the lowest since Q3 2006,

according to DTZ. 'In view of softening market demand, owners are more

realistic in asking prices,' it said.

The Sail @ Marina Bay got the strongest

subsale interest in Q3, with 30 deals (compared with 34 in Q2). The median

subsale price for the project slid 6 per cent quarter-on-quarter to $1,719

psf, following a 14 per cent slide in Q2.

Median subsale prices also fell 3 per

cent for Park Infinia at Wee Nam to $1,380 psf, The Esta (slipping 5 per

cent to $910 psf) and City Square Residences (down 6 per cent to $960 psf).

Mrs Ong expects subsales to continue

trending downwards although there will be spikes as major projects get their

TOP. That's when there's usually more sales activity as the finished product

can be viewed by potential buyers and the prospects of renting the units

would increase the appeal of such homes to potential investors.

- 2008 December 2 BUSINESS

TIMES

Singapore firms top wealth-creation

chart

They occupy

33 of leading 100 positions in Asean in a Wealth-Added Index; SingTel heads

the pack

Singapore companies have done a stellar

job of creating wealth for shareholders, despite market volatility and a

higher cost of capital.

The first-ever ranking of the top 100

South-east Asian companies in terms of US-based consulting firm Stern

Stewart & Co's 'Wealth Added Index' (WAI) finds a total of 33 Singapore

companies on the list, the largest number among Asean markets.

In pole position is Singapore

Telecommunications, as at June 30. Keppel Corp is ranked seventh, and

CapitaLand ninth.

Stern Stewart has also come up with the

top 100 WAI ranking for Singapore alone, as well as industry specific

rankings. In the regional real estate sector, for example, Singapore

companies accounted for eight of the top 10, led by CapitaLand and City

Developments.

WAI is a metric developed by Stern

Stewart in 2000, based on the idea that companies create value for

shareholders only if their total returns - share price plus dividends -

exceed an imputed 'cost of equity'. The latter is the minimum return

investors should earn for taking on the risk of investing in shares.

The strongest testimonial to the use of

the wealth added metric is Temasek Holdings, which on Monday released its

latest annual report. Temasek uses wealth added as an internal benchmark,

and that extends even to its staff compensation structure.

As Temasek explains: Wealth added (also

called economic profit) factors in the capital employed to produce the

returns and the risks associated with each investment. 'To achieve positive

wealth added, we need to deliver more than the capital charge, which is the

risk-adjusted hurdle applied to the capital employed.' In the year ended in

March, the group's wealth added was minus $6.3 billion. The group's

five-year cumulative wealth added was a 'healthy' $60 billion above its risk

adjusted cost of capital hurdle.

Erik Stern, president international of

Stern Stewart & Co, said the firm set up an office here in 1997 mainly

to work with the Temasek group. The firm maintained its office here for

about five years. It has since closed it, but is looking to re-establish

itself in the region.

'To people who want to know more about

economic value added (EVA) and the value mindset, I tell them to read the

Temasek annual report. There is nothing better. So many companies want to

look like they care about shareholder value. Read any annual report, then

read Temasek's. There is a very big difference.

'(Temasek) acts and lives it. We're

thrilled to be associated with them; they make us look good. They know what

this is all about.'

Stern Stewart first developed two metrics

in the 1980s, one of which is economic value added (EVA), focusing attention

on the cost of capital. EVA is a performance metric, to indicate whether a

company has produced value for investors. Its calculation takes after tax

operating profit and subtracts an annual charge - a sort of rental charge -

on debt and equity.

It is unclear how widely used EVA or

wealth added is among Singapore companies. SingTel uses a different metric

internally. CapitaLand, however, includes an EVA calculation in its annual

report, and tots up the group EVA attributable to equity shareholders.

Mr Stern said the metrics were developed

in an effort to overcome the limitations of other metrics, such as total

shareholder return, which simply measures the change in a company's price

plus dividends between two points in time.

Accounting measures like net profits and

sales also do not provide any benchmark for performance, or help in investor

decision making. 'The concept of EVA is like meritocracy; there is no

cutting corners. The objective is to get employees to think and act like

owners, so that they act like the money they're given is their own. That

concept is very similar to the Singapore mindset.

'I believe there is no accident that

Singapore companies' performance is good. People here are very modest. They

say, let's see what happens in the future, and there will be a lot of

competition..

'It pays to remember that capital has a

cost and shareholders deserve to earn a return on that. If Singapore

companies forget that they may find that the paradise they created will be

owned by others. As great as they've done, what matters is going forward.'

One point of contention may be the

calculation for the cost of equity, which is based on a market's government

bond adjusted by a company and market risk premium. Some of Stern's input

data are taken from Bloomberg.

Managers, he said, should focus on EVA as

an internal measure, and not the share price. 'Companies that consistently

make good decisions will see strong performance. The marketplace is showing

some fear of the future. The question is what can companies do about it.

'Companies that are well managed usually

do well in a downturn and take market share from those that are not well

managed.'

There are four drivers of wealth added,

which are quantified in the rankings. These are operations; strategy or

growth expectations; external financing and governance. The proxy for the

latter is a company's cost of equity.

'Our view of governance is that managers

must earn the required rate of return as the minimum. But if they don't earn

that, they have not been a good steward of capital.'

- 2008 August 28 BUSINESS

TIMES

Property firms report weak set of Q2

numbers

Most

developers see their business hit in 3rd and 4th quarters

Hit by

fewer home sales, lower revaluation gains from investment properties, drops

in divestment gains - and even the stronger Singapore dollar - property

companies largely reported weak results for the second quarter.

And the future doesn't look rosy either.

Most listed developers have warned that

the global slowdown and weakening market could hit their business in the

third and fourth quarters. Even the most upbeat are only 'cautiously

optimistic'.

The big three developers - CapitaLand,

City Developments and Keppel Land - all posted lower profits for Q2.

CapitaLand, Singapore's and South-east

Asia's largest developer, said its Q2 profit fell 43.5 per cent to $515.2

million, partly due to lower revaluation gains from investment properties,

lower portfolio gains and development profits, and the absence of previous

write-back provisions. Analysts called the results disappointing.

City Developments saw Q2 net profit drop

15.1 per cent to $165.2 million. Among other factors, CityDev was hurt by

the translation of its overseas hotels earnings at weakening exchange rates

due to the strengthening Singapore dollar.

Keppel Land reported that Q2 profit fell

16.4 per cent to $52.7 million as it sold fewer homes in Singapore and

abroad.

'I think the mood is generally very

cautious, and this has hurt the developers,' said an analyst. 'The trend is

likely to continue for the rest of the year.'

Right now, the fear is that sectors that

are currently contributing strongly to top lines, such as hospitality, may

soon start to weaken.

The Ministry of Trade and Industry's

latest quarterly economic survey showed there are increasing signs that

segments within services - including the retail trade and hotels - are

showing slower growth.

Property stocks with exposure to those

sectors - such as CapitaLand, CityDev and UOL Group, to name just a few -

could see contributions from those divisions drop.

For UOL, for example, a 4 per cent

increase in Q2 in revenue was due largely to hotel operations, with its

hotels in Singapore, Australia and Vietnam performing better.

As for the residential market here,

Citigroup has said prices of luxury homes could correct sharply, which could

have a negative impact on some developers.

'Scrapping of the deferred payment scheme

and tighter bank financing for investment properties may have also hurt

property transactions, which are off some 70 per cent from recent highs,'

Citi noted in a recent report. 'Some developers may have also over-committed

in terms of land purchases during the boom periods.'

Citi analyst Wendy Koh expects a 20-30

per cent price correction for high-end properties from their recent peak,

and reckons the mid-tier is likely to decline 10-20 per cent.

- 2008 August 15 BUSINESS

TIMES

Optimistic outlook for Asia-Pac

market, says DTZ report

Institutional investors are seeing some

property yield spreads over 10-year bond rates widen globally but DTZ

Research believes the correction in real estate markets has some way to go.

According to a recent DTZ Research

report, Money Into Property, the yield spread over the local 10-year bond

rate in Singapore increased by about one percentage point in the first

quarter of this year on a year-on-year (yoy) basis to just under 4 per cent,

and is higher than that in China and Japan, which both have yield spreads of

under 3 per cent.

While the high yield spread implies

growth potential and profitability in the real estate investment market, DTZ

Research did add, however, that Singapore is not immune from the weakening

global financial market outlook, with investors becoming increasingly

cautious.

DTZ executive director and regional head

for consulting and research Ong Choon Fah said: 'With prospects for capital

growth limited, investor focus has returned to occupier fundamentals.'

In Singapore, DTZ says that rentals for

prime office space in Raffles Place grew 1.1 per cent quarter-on- quarter (qoq)

to $19 per square foot per month in the second quarter of this year.

In the Shenton Way/ Robinson Road/Cecil

Street area, average rentals in Q2 increased 2.6 per cent (qoq) to $11.80

psf per month. In the HarbourFront area it's up 5.3 per cent (qoq) to $10

psf per month.

Rentals in Marina Centre and Orchard Road

were flat at $15.50 and $13.50 psf per month respectively.

DTZ said that the supply crunch in the

Central Business District will ease from 2010 with potential supply of new

office space from the second half of this year to 2013 estimated to be 12.1

million sq ft.

Already, the average islandwide occupancy

in the second quarter of this year has dipped slightly by 0.2 percentage

point (qoq) to 96.9 per cent.

Average occupancy of office buildings in

Raffles Place and Marina Centre dropped 0.3 and 1.2 percentage points to

97.4 and 98.6 per cent respectively.

Still, DTZ believes that the outlook for

Asia Pacific is relatively optimistic, supported by the occupier market and

improving investment access.

'Globally, we expect investment

transactions to be around US$500 billion in 2008, down 30 per cent on 2007.

This shift reflects weakness over the first half of 2008 and a relatively

modest pick-up thereafter, which is likely to be driven principally by the

Asia Pacific market,' added Mrs Ong.

Increases in yield spreads were greatest

in Europe with the UK seeing the biggest year-on-year rise of almost 2

percentage points in Q1 2008 to just under one per cent.

DTZ notes that the rate of fall in

capital values has been slowing in recent months in the UK, so that while

investment returns remain in negative territory, some improvement has been

evident.

According to DTZ estimates, investment

transactions in the UK appeared to stabilise in Q1, with the market's

relatively sharp repricing beginning to attract foreign-equity-based

investors, notably German funds.

At the same time, DTZ said an increasing

number of new opportunity (or 'vulture') funds have been set up to pick up

distressed assets in the UK market at bargain prices, while sovereign wealth

funds are also waiting in the wings.

- 2008 July 7 THE

BUSINESS TIMES

Singapore property market approaching

peak: report

Singapore is

still a safe haven for property investments but a market peak is

approaching, Pacific Star says in a recent report.

The Singapore-based property group is

most bullish on the retail sector here, recommending that investors add to

investments in that segment. The residential and office sectors, on the

other hand, are rated 'neutral'.

In the same vein, OCBC Investment

Research reiterated its 'neutral' view on the residential sector here in a

June 12 report.

According to Pacific Star, the retail

market here is tightening. Vacancy rates have fallen to levels not seen

since 1993 and rents continue to climb slowly, with an increase of one per

cent in Q1 this year, after a 0.6 per cent rise in Q4 2007.

Retail spending is expected to increase

in line with growing tourism and rising incomes.

'Marketing agents report that Orchard

Central and Ion Orchard, two prime (upcoming) shopping centres in Orchard

Road, are attracting strong rental enquiries from retailers that currently

do not operate in Singapore,' Pacific Star's report said. 'Rents at Ion are

expected to significantly surpass current prime retail rents.'

For the office sector, the current

demand-supply imbalance is expected to support rents till 2009, said Pacific

Star. 'Office demand is still firm with leasing agents lamenting the lack of

available space rather than a lack of enquiries, although the number of

enquiries would have fallen somewhat.'

But an above-normal supply of office

space will put pressure on rents from 2010, even if growing demand from the

services sector prevents any excessive correction, it said.

In the residential segment, Pacific Star

expects the current stupor to continue, as there are few catalysts for the

rest of 2008. It believes prices and transaction volumes will continue to

soften for the rest of the year.

However, the initial catalysts for

recovery are expected in 2009, when Singapore's economic growth is expected

to exceed that of 2008, according to Pacific Star.

The recovery will be fuelled by

immigration and higher incomes that will make it more affordable for

Singaporeans to buy mid and high-end private homes, it said.

In a report on the residential market

here, OCBC sounded a warning, saying past trends point towards another price

correction over the next few quarters.

On the other hand, interest in mass

market properties should come back, said OCBC.

'Given that only five projects with total

of 1,139 units are expected to be launched in the outside central region

between Q2 2008 and Q3 2008, this should ease concerns of oversupply and

drive the take-up rate higher over the next few quarters,' analyst Foo Sze

Ming noted. - 2008 June

24 BUSINESS

TIMES

Investment sales could hit $25b this

year

Despite the current subdued mood,

property investment sales this year could be substantial - about half of the

record $54.48 billion clocked last year, CB Richard Ellis estimates.

It bases the estimate on a tally of $5.91 billion of investment sales

deals struck in the first two-and-a-half months of this year.

'Assuming Q1 2008 ends with $6 billion, the full-year figure could be

around $24-25 billion. That would still be the third most active year on

record, after $54.48 billion in 2007 and $30.59 billion in 2006,' says CB

Richard Ellis executive director (investment properties) Jeremy Lake.

Investment sales are seen as a gauge of major players' confidence in the

sector's mid- to long-term prospects.

CBRE's definition of investment sales includes those with a value of at

least $5 million, comprising government and private sales, buildings and

land, strata and en bloc. It also includes change of ownership of real

estate via share sales.

It bases the estimate on a tally of $5.91 billion of investment sales

deals struck in the first two-and-a-half months of this year.

'Assuming Q1 2008 ends with $6 billion, the full-year figure could be

around $24-25 billion. That would still be the third most active year on

record, after $54.48 billion in 2007 and $30.59 billion in 2006,' says CB

Richard Ellis executive director (investment properties) Jeremy Lake.

Investment sales are seen as a gauge of major players' confidence in the

sector's mid- to long-term prospects.

CBRE's definition of investment sales includes those with a value of at

least $5 million, comprising government and private sales, buildings and

land, strata and en bloc. It also includes change of ownership of real

estate via share sales.

Mr Lake reckons momentum this year will be generated by the sale of

income-producing completed properties like malls, office blocks and

industrial buildings, as well as the sale of sites through the Government

Land Sales Programme, while the collective sales market has stalled.

'Continued strong growth in Asia, coupled with Singapore's position as a

financial services hub and popular business destination for MNCs, will help

maintain a healthy level of investment activity in the Singapore property

market,' CBRE said in a report issued yesterday.

CBRE's analysis shows the private sector made up 55 per cent or $3.27

billion of the $5.91 billion investment sales deals sealed in the first

two-and-a-half months of 2008.

Land sales by the public sector contributed the remaining 45 per cent or

$2.64 billion.

The biggest land deal so far this year was the award of a hospital site

at Novena Terrace/Irrawaddy Road to Parkway Holdings for $1.25 billion

($1,600 per square foot per plot ratio).

Splitting deal value by sectors, CBRE said the residential sector

accounted for $2.23 billion or 38 per cent of total investment sales.

'Compared with the heightened investors' interest in en bloc acquisition

witnessed in 2007, investors' demand for private residential land continued

to be lukewarm in the first quarter of 2008,' it said.

'Developers are no longer as keen to acquire more sites compared to last

year as most of them have built a relatively strong inventory of freehold

residential sites from the robust collective sales market in 2007.

'Developers have already taken the cue to act cautiously. The buying of

sites has been so far limited to specific choice sites since the response to

recent new launches has been subdued.

'In addition, the release of more affordable 99-year leasehold

residential sites by the government for sale in the first half of 2008 may

sway some buying interest away from prime freehold residential sites in the

private sector.

'The only successful collective sale deal in Q1 08 was Ban Guan Park,

which was acquired by Link THM Holdings for $31.10 million ($870 psf per

plot ratio).'

The office sector accounted for 34 per cent or $2.01 billion of

investment sales so far in 2008, on the back of big transactions like

Hitachi Tower for $811 million or $2,901 psf, Singapore Power Building

($1.01 billion or $1,820 psf) and One Phillip Street ($99.02 million or

$2,749 psf).

'Going forward, strong office demand and potential for further rental

escalation would lead to more acquisitions of office properties in 2008.'

CBRE said. 'The sustained influx of foreign investors should continue to

lead to steady activity in the office investment market.'

- 2008 March 18 BUSINESS

TIMES

New entrants flock in as property

sector booms

The property boom over the past two years

has drawn many new players who are looking to reap the high returns that

property development has to offer.

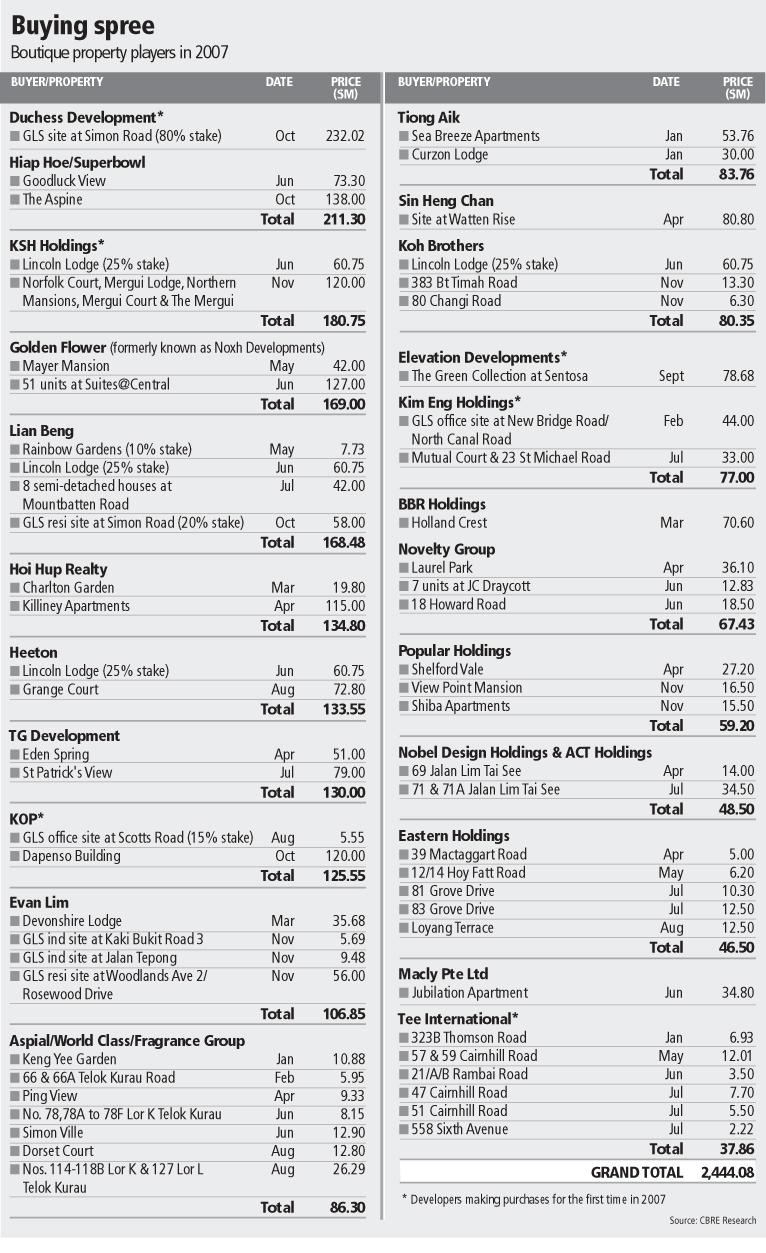

Six companies made their maiden property purchases

this year, data compiled by property firm CB Richard Ellis (CBRE) show.

Among them are companies that have made a name for themselves in other

businesses, such as construction company KSH Holdings and brokerage firm Kim

Eng Holdings. Others are lesser known, like Duchess Development which was

formed by two stockbrokers.

In addition, three other companies - BBR Holdings,

Popular Holdings and Eastern Holdings - first made their appearance in 2006

with land purchases. This year, they have gone on to snap up more sites.

'When the market is good, it draws in players who

may not have been active before,' said CBRE executive director Jeremy Lake.

He noted that many of the new entrants are

construction companies that might have decided to take on development risks,

after watching their developer clients reap big profits. During a property

boom, such risks are lessened.

'If you get your timing right in property, the

profits can be substantial,' Mr Lake said.

Experts said that the same trend was seen during

the last property boom, which lasted from 1993 to 1996.

Companies that did not look at property

development in the past are now beginning to do so because of the fatter

margins.

One example is SuperBowl, which teamed up with its

parent company Hiap Hoe to buy two sites for a total of $211.3 million.

SuperBowl's managing director Teo Ho Beng told BT

that while the company will continue to focus on its core leisure and

entertainment business, it will also increase its exposure to property

development where the margins are better.

Similarly, KSH Holdings sees good opportunities in

property development. The company's chairman and managing director Choo Chee

Onn said that his company invested in residential sites this year because

the opportunities opened up at the right time.

'Going forward, we will buy more sites if the

right opportunities arise,' Mr Choo said in an interview. The company spent

$180.8 million on two residential sites this year.

The first site, which KSH acquired in June with

three other partners, was the construction company's first purchase of a

land parcel.

Other companies branching out from their

traditional core businesses for the first time this year include electrical

and mechanical engineering firm Tee International.

However, new developers and developers looking at

boutique projects still account for only a small chunk of total purchases in

2007.

CBRE's data shows that the bulk of sites sold this

year went to big players such as companies linked to banker Wee Cho Yaw (UOL

Group, Kheng Leong, United Industrial Corp and Singapore Land), Malaysian

tycoon Quek Leng Chan's GuocoLand and property giant CapitaLand.

New and boutique developers together bought some

$2.4 billion worth of land sites in 2007, which account for about 5 per cent

of total investment sales so far this year.

In 2006, such developers accounted for about 4 per

cent of all investment sales, while in 2005, the figure was about 3 per

cent.

However, property analysts warned that these new

entrants are by no means guaranteed success. For starters, most bought sites

in the more central areas of Singapore, where the price gain is expected to

moderate this year even as construction costs are set to keep climbing,

leading to a drop in margins.

'For the high-end residential segment, there is

now risk of a potential correction,' said OCBC Investment Research analyst

Winston Liew.

New developers might not have the resources to

keep construction costs down unless they are contractors themselves, experts

said.

Next year, established developers who have carved

out niches are likely to do best, analysts said.

'Going into 2008, we look for developers with

specific niches and themes to outperform the sector as a whole,' said CIMB

property analyst Donald Chua. The research firm believed that listed

smaller-cap developers are likely to trade at a discount to target

valuations in 2008.

OCBC's Mr Liew advocated being defensive when

choosing property developer stocks. 'We prefer developers that are domestic

focused with substantial pre-sold projects, opportunities to unlock value

from investment properties and finally offering valuation upside,' he said.

- 2007 December 24 SINGAPORE

BUSINESS TIMES

Kuwait outfit snaps up 97 apartments

in $818m deal

Purchase of units in GuocoLand's condo under

development in Bukit Timah is biggest of its kind

Money spinner: GuocoLand's pre-tax

profit from the sale of the 97 units alone works out to around $500 million.

The company bought the former Casa Rosita site in April 2006 for $280

million or $706 psf per plot ratio

Foreign institutional investors continue to bulk buy apartments in new

residential developments in Singapore.

The latest deal - and biggest such transaction to

date - is Kuwait Finance House's $818.4 million purchase of 97 four-bedroom

apartments in GuocoLand's freehold condo, Goodwood Residence. The property

is being developed on the former Casa Rosita site.

The average unit price is understood to be

slightly over $3,000 per square foot. This is a new high for the prime Bukit

Timah area; it is about 25-30 per cent above the $2,500 psf average price

that Sui Generis is fetching at nearby Balmoral Crescent.

At over $800 million, the deal is the 'single

largest purchase of units in a Singapore residential project under

construction', says GuocoLand group president and CEO Quek Chee Hoon.

Industry observers' back-of-the-envelope

calculations show that GuocoLand's pre-tax profit from the sale of this

first batch of 97 units alone works out to around $500 million.

The four-bedders bought by a fund managed by

Kuwait Finance House (Malaysia) Berhad range from 2,500 sq ft to 3,900 sq

ft, GuocoLand said.

The Singapore property arm of Malaysian

tycoon Quek Leng Chan is likely to release the remaining 113 units in the

210-unit freehold condo for sale in the first quarter next year, depending

on market conditions. The development includes apartments with two and three

bedrooms, as well as penthouses.

The largest penthouse, a duplex unit of

about 12,000 sq ft with a rooftop pool, is expected to go for nearly $40

million. The WOHA Architects-designed project also includes 15 cabana-styled

apartments.

This is not KFH's first such investment

in the Singapore property market. A few months ago, an Islamic real estate

fund set up by KFH and the Malaysian government-owned Amanah Raya Berhad,

picked up two blocks (with a total of 56 apartments) at Reflections at

Keppel Bay for about $286 million.

Other recent foreign bulk purchases of

apartments in new projects here include Macquarie Global Property Advisors's

$136 million acquisition of 19 units at 8 Napier, at an average price of

$3,550 psf.

A Spanish private-equity fund is believed

to have bought 20 apartments at The Cascadia, further down Bukit Timah Road,

at about $1,600 psf.

While Singapore developers and property

consultants are cautious about prospects for high-end residential prices

next year - most are expecting modest gains of up to 10 per cent, after a

nearly 50 per cent spike this year - the outlook appears rosier to foreign

investors, market watchers say.

'From the perspective of these foreign

funds, they must place out monies they have raised. If they look at US,

there are sub-prime and credit squeeze problems. Growth in Europe is slow.

Frankly, they may not have a lot of options but to look to Asia,' the

research head of a property fund management outfit said.

Also, Singapore appears an island of calm

in a sea of turbulence, he said. 'It's relatively stable, will soon have the

integrated resorts and F1 attractions, and the island has positioned itself

as a wealth management hub - these are still important factors drawing

foreign institutional money to Singapore property.'

Goodwood Residence, which will comprise

two 12-storey blocks, is slated for completion in 2010.

The development has received the Building and

Construction Authority's Green Mark Award (Platinum). Goodwood Residence

will have more than 500 trees (including 58 preserved trees) planted in the

estate. In addition, the development site shares a 150-metre-long boundary

with the lush Goodwood Hill.

GuocoLand bought the former Casa Rosita site in

April 2006 for $280 million or $706 psf per plot ratio.

Other upcoming Singapore condo projects by

GuocoLand include Sophia Residence, with about 270 units, which the group

plans to release around Q3 next year, and an upscale development on the

Leedon Heights site that is slated for launch in 2009.

KFH is also co-sponsor - together with Singapore's

Pacific Star Group - of the Baitak Asian Real Estate Fund, whose major

investments include a stake in KL Pavilion, a mega development with luxury

residential, mall, office and hotel components in the prime Bukit Bintang

area of Kuala Lumpur. - 2007 December

19 SINGAPORE

BUSINESS TIMES

S'pore builders seen lagging Asian

peers

Policy risks,

fallout from sub-prime crisis may hurt property developers in 2008

Singapore's property companies may lag

behind Asian real estate developers for a second straight year in 2008 as

government limits on speculation cool the housing market.

CapitaLand Ltd, South-east Asia's largest

developer, is suffering its biggest quarterly decline in more than six years

after the government raised development charges by as much as 58 per cent.

The Singapore Property Equities Index has dropped 19 per cent so far this

quarter, the most since a 35 per cent plunge in the third quarter of 2001.

International buyers, who accounted for

more than 40 per cent of real estate purchases in 2006, bought 38 per cent

fewer properties last quarter as capital-market gridlock caused by rising US

sub-prime mortgage defaults curbed borrowing worldwide. The supply of new

homes for sale next year may almost double by value compared with 2006,

weighing on prices, according to CLSA Ltd.

'We can find better propositions

elsewhere in the region, where there's more growth and value to be found,'

said Leslie Phang, who helps manage US$1 billion at Commonwealth Private

Bank in the city. He does not own local builders and prefers Hong Kong

developer Sun Hung Kai Properties Ltd.

The decline in Singapore's property gauge

compares with a 10 per cent drop in the Bloomberg Asia Pacific Real Estate

Index, which tracks 164 companies. The Bloomberg World Real Estate Index has

slipped 8.9 per cent this quarter. Singapore's property index climbed 1.3

per cent yesterday, the biggest rise since Nov 29.

Singapore's home price index increased

8.3 per cent in the three months ended September from the second quarter.

That matched the June quarter's pace, the first time the growth rate failed

to rise since mid-2005.

Demand for apartments grew this year as

banks hired more expatriates. New York-based Morgan Stanley, the No 2

securities firm by market value, said in February that it would open a local

prime brokerage office servicing hedge funds. Citigroup Inc, the biggest US

bank by assets, followed with its own prime brokerage office in March.

About 19,200 jobs were created in

financial services through September this year, government data showed.

Foreigners accounted for about 43 per cent of total purchases in 2006, up

from 14 per cent in 2005, according to CLSA, the Asian investment-banking

arm of Paris-based Credit Agricole SA. Singapore home prices rose 13 per

cent last year, beating all other Asian markets, according to Global

Property Guide, a Manila-based researcher.

The number of foreign purchases fell 38

per cent to 2,073 last quarter, from a record high of 3,332 in the three

months ended June 30, according to DTZ Singapore, the local unit of DTZ

Holdings plc, a London real-estate brokerage.

The government scrapped a program on Oct

26 that allowed buyers of planned apartments to pay 10 per cent of the

asking price and defer the remainder until completion. Builders face higher

fees on new developments after the government raised charges by 58 per cent

for apartment projects and by 42 per cent for commercial properties,

starting Sept 1.

'There are still a lot of policy risks in

this segment,' said Daphne Roth, vice-president of equity research at ABN

Amro Private Banking in Singapore. 'The government doesn't want home prices

to go up too much, too quickly and the policy changes introduced so far have

already impacted the market.' CapitaLand has slumped 25 per cent in

Singapore stock exchange trading during the fourth quarter, set for its

biggest quarterly drop since a 47 per cent plunge in the three months ended

September 2001. It has lost 29 per cent after reaching a record high on Apr

26, even though third-quarter profit more than doubled from a year earlier.

City Developments Ltd, controlled by

billionaire Kwek Leng Beng, declined 18 per cent since the start of this

quarter and plunged 23 per cent from its all-time high on June 19.

The selloff has left local property

shares cheaper than their regional peers. The Singapore Property Index is

valued at 11 times earnings, less than a third of its high of 38 times in

March 2006. The Bloomberg measure of Asian real-estate stocks is valued at

19 times, while the global index is at 17 times.

Thue Isen, who helps oversee US$1 billion

at Bankinvest Group in Singapore, including shares of CapitaLand and City

Developments, said that the decline is a chance to buy local developers,

which he finds more attractive than those in Hong Kong and China.

'People's expectations for the property

market here have definitely dampened, which justifies some of those

declines,' he said. 'If you look at economic and income growth and new

offices starting up, the fundamentals haven't changed that much, so the

pullback looks a bit excessive.'

CIMB-GK Research, based in Singapore, cut

its price forecasts in a Dec 10 note. Properties costing at least S$1,200 a

square foot may climb 8 per cent in 2008, compared with an earlier forecast

of 15 per cent. Overall home prices will rise 15 per cent from a previous

estimate of a 25 per cent increase, said Donald Chua, a Singapore-based

analyst.

The brokerage, a unit of CIMB Bank Bhd,

Malaysia's largest investment bank, also cut its rating on the industry to

'underweight' from 'overweight', citing slowing growth. The firm lowered its

recommendation on CapitaLand to 'neutral' from 'outperform'.

CLSA forecasts that as many as 12,000 new

homes under construction could be up for sale in the next year to 18 months

in the most expensive residential districts, driving up supply and hurting

prices. The 'unprecedented' inventory is worth S$21 billion, almost twice

the S$11 billion invested in real estate in 2006, according to Yew Kiang

Wong, a CLSA analyst in Singapore.

'There's just too much negative news out

there right now, with the government regulations and concerns over

sub-prime,' said Nicole Sze, Singapore-based investment analyst at Bank

Julius Baer, which manages US$350 billion. 'We're unlikely to see the same

kind of broad-based rally that we've had.'

- 2007 December 20 BLOOMBERG

Circle Line key to higher plot ratios

Study

looks at how Master Plan 2008 could change landscape, usher in new

initiatives

When Master Plan 2008 is unveiled

sometime this year, certain areas are likely to see an increase in plot

ratios. A study by Jones Lang LaSalle has tried to zero in on which areas

could be allowed more intensive use of land.

Its conclusion: Look out for undeveloped

state sites within walking distance of Circle Line MRT stations,

particularly those that intersect with existing MRT lines. They are the top

candidates for higher plot ratios.

The property consulting group

specifically highlighted the areas near Paya Lebar MRT Station, Buona Vista

MRT Station (which will see the Circle Line intersecting with the existing

East-West Line) and HarbourFront MRT Station (Circle Line crosses North-East

Line). Also, while Buona Vista is shaping into an R&D/commercial hub,

the HarbourFront district's redevelopment potential is increasing because of

projects in Sentosa and Keppel Bay nearby.

Another promising area is in the vicinity

of the Circle Line Station at Telok Blangah. Although it does not intersect

with an existing MRT line, it will benefit from a spillover from the ongoing

redevelopment in Sentosa and HarbourFront.

JLL does not see major, across-the-board

increases in plot ratios in MP 2008. But it argues that intensifying land

use for undeveloped state plots along these stations will spread social

benefits from the government's investment in the Circle Line to more people

and also improve accessibility.

Raising plot ratios (ratio of maximum

potential gross floor area to land area) will also address the issue of

rising demand for Singapore's properties and prevent overcrowding in

specific areas such as the central and CBD regions.

Although the Circle Line also touches

locations near Dhoby Ghaut and Bishan MRT stations, JLL excludes them as

these areas already have high plot ratios.

The study also suggests that white sites

- with a range of uses and change in use mix allowed - will be more readily

available islandwide instead of being confined largely to the CBD. 'It

further promotes creativity in future projects,' says JLL's head of research

(South-east Asia) Chua Yang Liang.

He also sees the Urban Redevelopment

Authority introducing more mixed use, rather than traditional single-use

zones, to 'further provide the flexibility needed to accommodate changing

demand patterns as a result of shifting demographics'. MP 2008 could also be

more tolerant of non-traditional types of residences. For instance, obsolete

industrial buildings could be re-modelled along the lines of New York's

Manhattan lofts. 'This will accommodate shifting market forces and tastes,'

Dr Chua argues.

JLL also suggests that URA may realign

traditional industrial estates to support demand needs of the

knowledge-based economy or rezone them for other uses. 'For example,

industrial areas within housing estates such as those found in Jalan

Pemimpin could potentially be rezoned to residential or possibly an

education hub,' it said. After all, the area is near Raffles Institution and

Raffles Junior College.

MP 2008 could also extend the 'work, live

and play' concept beyond Marina Bay into the suburbs as Singapore cannot

live by its business image alone, JLL predicts. 'We can expect to see more

areas designed for cultural developments, for example, the civic, cultural

and retail complex in Buona Vista, and new conservation areas that serve to

retain the fabric of the collective memory,' Dr Chua said.

JLL also expects to see many more

recreational zones across Singapore. 'The likes of the recent Punggol

announcement will be more common,' the study said.

On the back of Sentosa Cove's success,

JLL expects other islets around Singapore like Southern Islands and Pulau

Ubin to be put for waterfront residential use.

In the existing CBD, JLL suggests that

Shenton Way will see a further shift towards a mixed-use (including

residential) district, once the current office supply crunch eases. In May

last year, URA announced a temporary ban on conversion of office use in the

central area, including the CBD, to other uses until end-2009.

Last year, the government identified

Jurong East and Paya Lebar for development into business hubs. Dr Chua says

land around Paya Lebar MRT Station will be intensified in line with

government plans to transform it into a sub-regional centre and that the

location will be ideal for cost-conscious office tenants.

However, Dr Chua suggests that the area

around Jurong East MRT Station is more suited for research and development

because of its proximity to universities, the Science Park and one-north

rather than as an alternative backoffice hub along the lines of Tampines.

National Development Minister Mah Bow Tan

last year also ruled out massive, across-the-board islandwide increases in

plot ratios for MP 2008 to cope with a higher population target of 6.5

million. The Master Plan, a detailed land use plan that guides Singapore's

medium-term physical development, is reviewed every five years.

- 2008 January 4 SINGAPORE

BUSINESS TIMES

RESIDENTIAL

Property boom expected to continue

Robust economy, jobs growth, strong housing demand and en bloc sales

proceeds are key drivers

The bullish sentiment in Singapore's

residential market continued into 2007 from where it left off in 2006. In

the first nine months of this year, the market recorded a total of 29,331

sales transactions worth some $52 billion. This represents a year-on-year

increase of 89 and 116 per cent respectively.

The demand for high-end residential housing has been growing at a

feverish pace over the past two years and although the stock market plunge

may have affected investor sentiment, new benchmark prices continued to make

headlines over the past two quarters. Rising fast to support the high-end

residential sector are the mid-tier and mass market segments, which have

picked up significantly since early 2007 with record prices set at several

project launches. Strong economic outlook, coupled with higher salaries and

bigger bonuses and rapid jobs growth have brought new impetus for investors,

home owners and speculators to upgrade and/or to purchase.

Comparing average prices with those at the end of 2006, the average price

for homes in the super luxury market segment (luxury developments which

crossed the $2,500 psf mark in Q4/2006) jumped 42 per cent to $3,700, while

the high-end market segment (luxury developments in Districts 1, 4, 9, 10

& 11) rose by 36 per cent to $2,076 per sq ft. The average prices for

both mid-tier and mass market developments have also risen by more than 50

per cent, albeit from a lower base, to $1,250 per sq ft and $700 per sq ft

respectively.

One major market driver is en bloc sales, which have been very active

since early 2005. However, with the prolonged US sub-prime credit woes,

hikes in development charge rates and the tightening of en bloc sales

legislation, the en bloc sizzle has taken a breather from the end of the

third quarter of this year.

This has been a phenomenal year for en bloc sales. Since January, some 95

en bloc sales with a total value of $11.3 billion were transacted, compared

to 65 transactions totalling $7.5 billion for the whole of 2006. The

displaced tenants and owner-occupiers from these properties have contributed

to the overall increase in rentals and capital values of homes in the

mid-tier, mass and public market segments.

Notwithstanding the stock market shock in the third quarter, the buying

momentum is expected to resume between next month and early 2008 given the

wave of purchases from displaced en bloc-owners who are expected to collect

their money and buy a replacement home around this time. This time round,

the mid-tier and mass market segments will lead the way with a strong

growth, lending solid fundamentals to prices in the high-end and luxury

sectors.

For next year, the residential market in Singapore is expected to remain

strong with all segments looking set to continue growing supported by robust

domestic economy, jobs growth, wage growth in both the public and private

sectors, strong housing demand from expatriates relocating to Singapore and

reinvestment of proceeds from en bloc sales.

The general market consensus is that supply will tighten due to a short-

term supply crunch in 2008, as the expected demolitions from en bloc sales

outstrip the completion of new projects. The tightness in supply will be

exacerbated by the need to fill job vacancies which stood at close to 40,000

by mid-2007 with unemployment standing at 1.7 per cent in September 2007.

An estimated 10,000 units from en bloc sales are also expected to be

demolished in 2008 while TOPs from new projects are expected to re-supply

only 8,000 units. (This is largely due to the few construction starts back

in 2003 and 2004 when economic confidence was low, which resulted in low

completion numbers in 2007 and 2008.)

Furthermore, there is also the potential risk for a slower pace of

construction of residential properties arising from the strong competition

for resources in the construction sector. This is largely due to the fact

that several of these mega projects are also scheduled for completion within

the next three to four years. Some of these mega projects include the two

integrated resorts, BFC, petrochemicals plants in Jurong Island, public

infrastructure such as the Circle Line and Circle Line Extension, common

services tunnel in Marina Bay, sports hub at Kallang, and Gardens by The

Bay.

On the demand side, there are several significant events that could spur