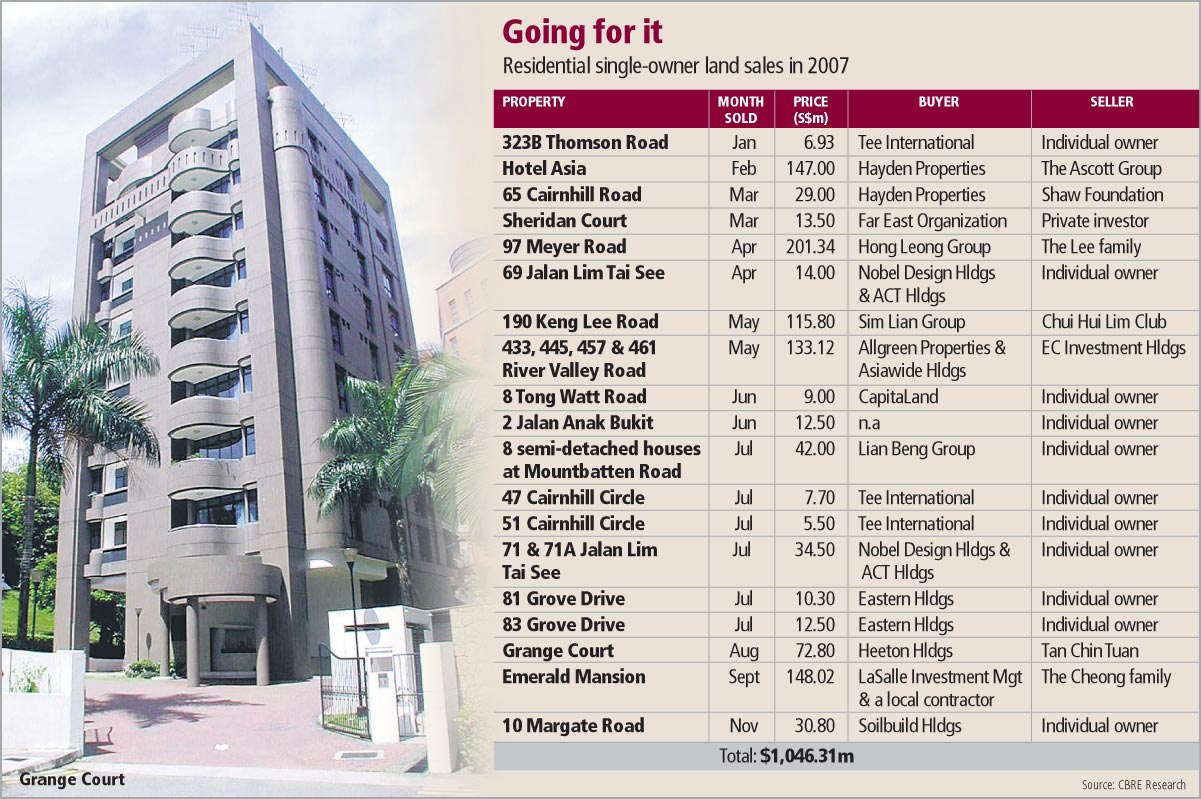

|

RESIDENTIAL

SITES

19 single-owner plots worth

$1.05b sold in 2007

With the property market running hot, it is not just collective

sales that have ballooned. Over the past two years, more residential

land sites owned by single owners were sold as well.

So far this year, 19 residential sites owned by single owners and

worth some $1.05 billion in all were sold to developers, data provided

by property firm CB Richard Ellis (CBRE) shows.

And in 2006, there were 15 single-owner land sales worth a total of

$865 million. By comparison, just four single-owner land sales worth

$303 million were done in 2005.

Market watchers say a property market that is strong and active

will bring out more sellers - both of the en-bloc variety as well as

single owners.

'Collective sales have hogged the limelight of late, but the

single-owner sales have also been very active,' says CBRE executive

director Jeremy Lake. 'If you look at overall residential sales, you

will see that they have gone up too. So single owners are just

mirroring the overall market.'

Ku Swee Yong, director of marketing and business development at

Savills Singapore, says that in the case of those sites owned by

associations or clubs, members who were looking to sell might have

been able to convince those who were previously not in favour of

selling to change their minds, considering the prices that the

properties can now fetch.

'When the price is better, they (those looking to sell) manage to

clear the hurdle,' Mr Ku says.

The 19 sites sold by single owners this year include a few owned by

associations, including one sold by Chui Hui Lim Club. The club sold a

Keng Lee Road site to Sim Lian Group for some $115.8 million.

CBRE's data also shows that this year, while there were a few large

single-owner sites that were sold, the bulk of the 19 properties were

small - with 10 of them going for less than $30 million each.

Market watchers attributed the increased interest in smaller sites

to new players in the property market. These smaller developers

generally do not have the resources to bid for en-bloc sites that go

for hundreds of millions dollars - the province of the likes of

CapitaLand, City Developments and foreign property funds.

'When the market is good, it will attract new entrants,' says

CBRE's Mr Lake. 'And you will find some people who will want to get

into the market, but might not be able to afford the big sites.'

Sesdaq-listed Tee International is an example of one new entrant

which has been snapping up smaller sites. The company, which has a

market capitalisation of $41.5 million, has been in the electrical and

mechanical engineering business since 1980. But since the start of the

year, Tee has been buying a string of freehold terrace houses and

apartments with plans to develop them into luxury 'boutique' homes.

Among its purchases are three single-owner sites, CBRE's data

shows. Tee acquired two single-owner plots in Cairnhill Circle in July

- one for $7.7 million and the other for $5.5 million. It also bought

a single-owner property in Thomson Road for $6.9 million in January

this year.

Similarly, Eastern Holdings, which publishes magazines, also picked

up two small single-owner sites in Grove Drive this year - one for

$12.5 million and the other for $10.3 million. The company is also

relatively small, having a market capitalisation of about $70 million.

Savills's Mr Ku says that there are also some high net worth

individuals who are buying smaller sites, redeveloping them and then

selling them - all within a short span of time - to capitalise on the

property market.

These wealthy individuals were also adding to the demand for

smaller sites, he says. - 2007 November

22 SINGAPORE

BUSINESS TIMES

Amendment to Land Titles (Strata)

Act

It will extend en bloc sale by

majority consent to five more developments

A proposed amendment to the Land Titles (Strata) Act will extend en

bloc sale by majority consent to five developments not covered by

current legislation - Goldhill Plaza, Goldhill Shopping Centre, Katong

Plaza, Roxy Square Shopping Centre and Bukit Timah Shopping Centre.

Strata title certificates were issued for the projects but the

original landowner/developer retained the title certificates and

instead gave long leases - at least 850 years - to buyers of units.

Owners of such units can only do an en bloc sale with unanimous

consent - and the approval of the original developer, who owns the

reversionary interest in the property.

But the ministry of law proposes to allow them to proceed with an

en bloc sale by majority consent.

And the original developer's consent will not be required, because

if the Strata Titles Board approves an en bloc sale, he will lose all

rights to the land. - SINGAPORE

BUSINESS TIMES 2007 August 28

Ang Mo Kio condo site sets record

Far East's $202.9m winning bid means suburban project may

eventually launch at over $1,100 psf

A plum condominium site in the

heart of Ang Mo Kio has set a new record for suburban land prices,

fetching some $601 per square foot per plot ratio (psf ppr).

And when the project is eventually launched, it could set a record

for private home prices outside the central areas, analysts said.

Yesterday, HDB said that Far East Organization put in the top bid

for the 0.6-ha mass market condo site at Ang Mo Kio Avenue 8. The

developer beat 13 other bidders with its bullish offer of $202.9

million - which works out to $601 psf ppr .

'The price is probably the highest paid for a suburban site in

recent years,' said Donald Han, managing director of property firm

Cushman & Wakefield.

Analysts said that Far East's bid for the 99-year leasehold site

beat market predictions that the top bid would be around $500 psf ppr.

Far East's break-even cost for the site is now estimated to be in

the region of $900-$1,000 psf, which means that units in the project

could eventually be launched at $1,100-$1,200 psf - a record for

private home prices in the suburbs.

'If Far East can achieve prices of around $1,200 psf for the

project, then yes, it will be a record for the suburban areas,' said

Ku Swee Yong, Savills Singapore's director of marketing and business

development.

By comparison, units in other projects in the vicinity - albeit in

less attractive locations - are mostly going for around $400-$600 psf.

Far East's bid was 11.8 per cent higher than the next highest bid

of $538 psf ppr put in by Chip Eng Seng.

The bid was 68.9 per cent higher than the lowest bid of $356 psf

ppr bid jointly put in by Wing Tai Holdings and United Engineers.

Far East also beat out other big names such as CapitaLand, Hong

Leong Group and Frasers Centrepoint.

Experts said that the high prices and large number of bids

signalled that developers had confidence in the strengthening suburban

residential market - notwithstanding the US sub-prime mortgage fears

that rattled stock markets here.

The plot also drew strong interest due to its good location. It is

situated right next to Ang Mo Kio MRT station, and is just 15 minutes

away from Orchard by train.

'With an increase of 4.2 per cent in overall HDB resale prices in

the past six months, more HDB households would be poised to upgrade to

this conveniently located private development,' said Li Hiaw Ho,

executive director at CB Richard Ellis' research unit.

Units in the project could be sought-after by HDB upgraders in the

Bishan and Toa Payoh estates - where HDB resale prices command a

premium - as well as Ang Mo Kio itself, Mr Li said.

I n addition, the project may also prove to be attractive to private

homeowners in Serangoon and the Thomson/Upper Thomson Road areas, he

added.

The site, which was on the government's reserve list, was launched

in July after an unnamed developer bid $102 million, or $302 psf ppr

area for it. - SINGAPORE

BUSINESS TIMES 2007 September 12

Pinetree condo put up for sale

Indicative price for the 12-year-old freehold site in Balmoral Park

is $140m to $150m

Pinetree Condominium

in Balmoral Park has been put up for sale by tender with an indicative

price of $140 million to $150 million.

|

| Pinetree Condominium:

Based on a sale at $140 million, the 41,361-square-foot property

will cost about $2,100 per square foot per plot ratio |

The freehold residential

redevelopment site in district 10, which is about 12 years old, was

put up for sale through an expression-of-interest exercise in April

last year.

The indicative price then was about

$59 million. This represents an increase in price by about 11/2 times.

More than 80 per cent of the owners

have now agreed to the collective sale.

The block is being marketed by

Jones Lang LaSalle, whose regional director and head of investments

Lui Seng Fatt said: 'There have not been many collective sale sites in

the exclusive Balmoral Park area and with the recent hike in

development charge, Pinetree Condominium, which has no development

charge, will be an attractive site for developers to consider.'

Mr Lui said there would be no

development charge payable as the current gross floor area is

maximised.

Based on a sale at $140 million,

the 41,361-square-foot property, which can have an estimated gross

floor area of up to 66,178 square feet, will cost about $2,100 per

square foot per plot ratio (psf ppr).

Mr Lui added that the site can be

combined with the adjoining landed properties to form a total

potential land area of approximately 68,633 sq ft, which would yield a

total combined gross floor area of 109,800 sq ft.

Based on this size, a developer

could build a new development consisting of 70 to 80 luxury apartment

units. Mr Lui estimates a break-even price of about $3,100 psf.

Some benchmark prices in the same

area include those of The Solitaire, which has had a few transactions

done above $2,200 psf, and Orange Grove Residences, which had

transactions ranging from $2,100 to $2,350 psf.

- by Arthur Sim SINGAPORE

BUSINESS TIMES 2007 September 11

Smaller players grabbing slice of

prime real estate pie

So who

says only the 'big boys' have fun?

|

| Hot

property:

Sing Holdings' Cairnhill Road acquisition cost the Sesdaq-listed

company $361 million |

Last Friday, it was widely reported

that Sesdaq-listed Sing Holdings had bought a prime Cairnhill Road

property.

Sing Holdings, with a market worth

of some $97 million, bought its Orchard area property for $361

million, or $1,542 psf per plot ratio.

But Sing Holdings is not the only

secondliner in the profitable-plots game.

Heeton Land and builder Koh

Brothers are among a growing list of smaller players which are also

sitting pretty on prime real estate, putting them in the same arena as

the big boys like SC Global Developments, City Developments and Wing

Tai Holdings.

Sesdaq-listed Heeton, which started

out in 1976 running fresh food markets, partnered mainboard-listed Koh

Brothers last April - when the residential property market was still

in deep slumber - to buy Hilton Towers in Leonie Hill for $79.2

million, including a development charge of $3.9 million.

Each party has a 50 per cent stake

in the 33,700 sq ft freehold district 9 estate.

Property market insiders estimate

that the property has a breakeven level of about $1,300 psf, assuming

construction cost of around $350 psf.

Given the recent pricing in the

vicinity, an up-market condominium to be built there could fetch

upwards of $2,000 psf.

Even this may be conservative,

given the recent prices of other properties in the Orchard vicinity.

Sing Holdings, which has a breakeven cost for its Cairnhill plot in

the region of $2,000 to $2,100 psf, expects a minimum sale price of

$2,300.

Nevertheless, even at a

conservative $2,000 psf, and given the gross saleable area of some

120,000 sq ft (assuming over 50 units), Heeton and Koh Bros would rake

in total gains in excess of $80 million.

This would be a remarkable

achievement for two companies whose earnings are around $5 million

each: Heeton recently reported FY06 earnings of $4.5 million, while

Koh Bros posted $5.3 million.

Heeton, which has a market value of

$100 million and whose other investments include Sun Plaza (which it

jointly developed with Koh Bros) and some 200 wet market stalls

islandwide, recently proposed a placement of up to 21 million new

shares at an issue price at 33 cents per share to raise a net $6.67

million.

Koh Brothers' previous projects

include The Montana off River Valley Road and The Sierra in Mount

Sinai, and it also bought Alocassia Apartments on Bukit Timah Road

last year.

Other smaller players that have

been getting into the property game over the past year include BBR

Holdings, Sim Lian Land and Chip Eng Seng.

- 26 March 2007 SINGAPORE

BUSINESS TIMES

Dragon View Park condo (En bloc) Site

Owners at

Dragon View Park are hoping it will be third time lucky for them. The

freehold condo at River Valley is up for collective sale again.

This time the owners have lowered their expectations to $125-128

million, down almost 30 per cent from $175 million in 1999. BT

understands owners at the 88-unit development had tried to do an

en-bloc sale in 1997 but fell short of the required number of

consenting owners.

At $125 million to $128 million, this works out to a land cost of

$517-529 per square foot (psf) of potential gross floor area,

including an estimated development charge of $11 million. While lower

than the asking price in 1999, the owners can still pocket generous

premiums of 40-50 per cent over what they can expect if they sold

individually.

The site with a land area of 125,133 sq ft can be built up to 2.1

times. Developers can build a 24-storey condominium with some 250

units. Break even is estimated at $790 psf.

Comparable to Dragon View Park are the former Times House site sold

to Marco Polo and Quelin Gardens at St Thomas Walk. Marco Polo paid

$118.88 million for the Times House site or $450 psf per plot ratio (ppr)

inclusive of an estimated development charge of $23 million. Chip Eng

Seng forked out $79 million or $490 psf ppr for Quelin Gardens.

The en bloc sale of Holland View has cleared

its final hurdle, after two owners who argued against it settled their

case before it was brought to the Strata Titles Board (STB) for

mediation, sources say.

(Dragon View Park) development site is one of the last few

remaining sizeable plots available for sale in Singapore's prime

District 10,' said Colliers International director of investment sales

Ho Eng Joo. 'Located on high ground off a quiet cul de sac of River

Valley Road with unobstructed city views and with residential prices

in the third quarter showing signs of recovery, this site will be a

popular choice for developers looking to beef up their prime land

bank.'

The existing development comprising two blocks was completed in

1968. Back then, units in the lower four-storey block were sold at

$38,000 each, while those in the adjacent 14-storey tower went for

$45,000 each.

The tender will close on Nov 2. - by

Andrea Tan SINGAPORE

BUSINESS TIMES 7 Oct 2004

|

| 46 Holland View:

On average, owners stand to get 50% more from the collective sale. But

after taking into account such costs as mortgage interest charges,

renovation, stamp fees, the two owners claim they would suffer a loss.

|

The owners are understood to have objected

to the sale because, among other things, they would suffer losses

after taking into account costs such as mortgage interest charges,

renovation costs, property taxes and stamp fees. The treatment of

these cost elements is ambiguous under the Strata Titles Act.

The Holland View sale was to have been a

landmark hearing before the STB as it has never been stipulated what

deductions are allowed in the calculation of an owner's profit or

loss. Any firm ruling could impact future en bloc sales, raising

questions such as whether lavish renovations are justified as a factor

contributing to an owner's loss.

For the en bloc sale of an estate of more

than 10 years old to succeed, 80 per cent of the owners must agree to

a sale. Holland View is 19 years old, and close to 95 per cent of

owners have agreed.

But in any en bloc sale, an owner who stands

to make a loss can apply to the STB to have the deal vetoed. It was

reported that the owners of Holland View will, on average, get 50 per

cent more from the collective sale than if their properties were sold

separately on the open market.

It was announced in April that listed

construction and property group Sim Lian had clinched the estate for

$61.68 million. This means the owners could reap $770,000 to $1.4

million, depending on the size of their units.

Meanwhile, Jones Lang Lasalle, who brokered

the Holland View deal, said yesterday that two new sites in the River

Valley area, including the 16-unit Nathan Court, are up for tender.

They can be bought separately, or as one site measuring over 23,300

square feet. The tender closes on Nov 9.

Analysts believe the single plot could fetch

around $450 psf of potential gross floor area. Break-even cost for

developers would be around $700 psf.

New homes in the area are selling at an

average of over $800 psf, consultants say. This means that Nathan

Court owners may reap premiums of more than 50 per cent over what they

would be able to get selling individually.

Said JLL associate director: 'If a buyer

successfully acquires both parcels, the combined site would be able to

yield an estimated gross floor area of approximately 65,300 sq ft,

subject to payment of development charge.' - by Vince

Chong SINGAPORE BUSINESS TIMES

5 Oct 2004

En bloc market braces for

Holland View outcome

Signed but not sealed. The collective sale

of Holland View is set for a landmark hearing by the Strata Titles

Board (STB) in about two weeks, which could lead to implications for

the entire en bloc market.

Sources told BT yesterday the deal will go

before STB after two of the 46 owners objected to the sale on the

grounds they will suffer a loss.

It will be the first such hearing on this

issue. Similar cases have come up before but have been settled

privately, without dragging STB into the matter. And things could turn

out this way with Holland View, given the hearing is still some time

away.

The two owners are allegedly objecting to

the sale because, among other things, they would suffer losses after

taking into account costs such as mortgage interest charges,

renovation costs, property taxes and stamp fees. All of these factors

are ambiguous under the Strata Titles Act.

For the en bloc sale of an estate more than

10 years old to succeed, 80 per cent of all owners must agree. Holland

View is 19 years old, and close to 95 per cent of owners have agreed.

But in any en bloc case, an owner who stands

to make a loss can apply to STB to have the deal vetoed.

Observers say the Act defines an owner's

loss as 'the proceeds of the sale of his lot, after any deduction

allowed by the Board, (being) less than the price he paid for his

lot'.

However, what is deemed an allowed deduction

has not been clearly set out. And any firm demarcation on this by STB

in the Holland View case could complicate future en bloc sales.

For example, as one owner involved in

another en bloc sale asked: Can renovation costs be justified as a

factor contributing to a loss if someone has upgraded their home with

lavish but unnecessary fittings and built-in furniture.

The Collective Sale Agreement signed by 46

Holland View owners defines any profit or loss as the 'difference

between the original purchase price and the gross sales proceeds of

the unit'. Based on this definition, sources say both owners are in

the money. On average, owners will get 50 per cent more from the

collective sale than their properties could fetch on the open market.

It was announced in April that listed

construction and property group Sim Lian had clinched Holland View for

$61.68 million in an en bloc deal brokered by Jones Lang Lasalle. This

means owners could reap $770,000-$1.4 million on their homes,

depending on size.

Consultants expect eight to 10 en bloc sales

this year, after eight such deals totalling $577 million were

concluded in 2003. - by Vince

Chong SINGAPORE BUSINESS TIMES

21 Sept 2004

A crippling blow for property

owners

Policy of upping plot ratios only on empty land changes rules of game

Last Friday Dr Vivian Balakrishnan, a medical doctor and hospital

administrator turned politician, made an announcement that drove a stake

through the heart of the property market. And he did it with a smile.

Speaking at the launch of the draft west region Master Plan, part of a

blueprint for Singapore's future physical development, he said the government

will raise plot ratios for residential land near 'public transport nodes'.

But this will be done selectively and only land currently empty will

benefit from the higher plot ratios, which allow for more intensive

development. This is to 'enable areas that have already been built-up to be

left intact, so that the estate's established character can be retained', he

said.

Dr Balakrishnan, the No 2 man at the National Development Ministry, is an

accomplished debater. Perhaps his audience was lulled by his voice. Perhaps

they were more concerned with the government's Budget announcement on the same

day. Whatever the reason, few realised that he had quietly changed the most

fundamental rule of the property market.

Property is 'location, location, location'. More than anything else,

location decides the value of a property. With the right location, a shop will

get more customers, a hotel more guests, a condominium a better class of

tenants and a factory more willing workers. Get it wrong, and nothing else -

be it design, facilities, or other factors - will be enough to compensate for

the disadvantage.

This may no longer be true in Singapore. In his soft, even voice, Dr

Balakrishnan in effect disclosed that location will no longer be the main

criterion for value, because properties in the same area may not be treated in

exactly the same manner anymore.

Take the policy on plot ratio. It used to be that a higher plot ratio

benefits all properties within a prescribed area. Now the windfall only goes

to empty land, and a block of condos may stand between two vacant lots and

still be denied the higher plot ratio given to its neighbours.

Private property owners are certain to be upset. They will also point out

that it is the government that will benefit most from the change as almost all

vacant land in Singapore is owned by the state.

Markets thrive on certainty and transparency and the new policy Dr

Balakrishnan unveiled has robbed the property market of both.

The market is no longer certain, as the rule change will result in

different parties benefiting differently.

And it is not transparent because no one knows how the new rule on empty

land has come about.

Previous bad call

One guess in the property market is that the Urban Redevelopment Authority,

author of the Master Plan, may have misjudged badly when it last raised plot

ratios in the mid-1990s.

Those inclined to this view cite various examples as evidence. Higher plots

ratios were given in URA's design guide plans, but were disallowed when owners

tried to put them into practice.

There is also a strange policy that allowed high-rise redevelopments in the

central, crowded areas, thus causing more congestion, but not in outlying

areas where high-rise developments would do less harm.

And, of course, by limiting the higher plot ratios this time round to

owners of empty land, it is hard to avoid the conclusion that the beneficiary

will be mostly the government.

So what next for a property market that is no longer as certain and

transparent? The answer is simple. Like all markets that have lost their

direction, it is likely to soon see the departure of investors.

In Singapore, most property owners are stuck with their properties and

cannot leave. But the fortunate ones who can may soon pull up stakes and put

their money in greener pastures.

After all, what's the point of investing in a market where you might wake

up one morning and find yourself disadvantaged by a new set of rules?

- By Lee Han Shih SINGAPORE BUSINESS TIMES

04 Mar 2003

King's and Queen's Flats

Kim Tian Road off Tiong Bahru Road

JLL has finally closed the en bloc deal on King's and Queen's Flats after

seven long years and three launch attempts.

The property firm yesterday confirmed earlier BT reports that the two

estates - totalling 112 units of mostly smallish apartments - were sold at a

hefty $82 million. At an average of $500,000-$900,000 a home, based on

simple calculations, this represents a whopping estimated premium of at

least 60 per cent over market prices, said JLL.

This is similar to the heady days of the collective sales market, when

premiums were at least 40 per cent.

Premiums of 50-70 per cent were common with some owners enjoying rates of

100 per cent or more.

Located in an older part of the city on Kim Tian Road off Tiong Bahru

Road, the majority of the flat owners are understood to be in their 70s and

80s.

JLL country head said: 'The sale price comprises $21 million for King's

Flats (32 units) and $61 million for Queen's Flats (80 units). Should the

developer choose to develop the site into a 20-storey condo with full

facilities, more than 170 units averaging 1,200 sq ft per unit can be built

on site.'

Market watchers said that attempts at selling the estates, where units

range from 753-1,284 sq ft, began in 1996.

A consultant said: 'An en bloc deal takes an average of three to four

years from start to completion, so this deal has indeed been literally a big

deal to some who have been involved from the beginning.'

JLL also confirmed BT's earlier report that the buyer of King's and

Queen's Flats is a joint venture comprising United Overseas Land - which

developed Tiong Bahru Plaza nearby - and its long-time partner, listed

construction group Low Keng Huat.

The flats, close to Tiong Bahru MRT station, have a combined freehold

site area of about 82,400 sq ft. At $82 million, land cost comes to over

$340 per sq ft of potential gross floor area.

A minimal development charge is payable as the sites have a high

development baseline, BT understands. A new condo on the site could break

even for below $700 psf, say analysts.

The last attempt to sell the flats was in October 2000, JLL said, which

was subsequently withdrawn following the market downturn.

JLL had also concluded last year's biggest en bloc sale, Lengkong

Gardens, worth $49.5 million. - by Vince Chong

Singapore

Business Times 15 Feb 2003

Parkview Condo to go on en bloc sale for $200m

956-year leasehold plot is biggest site offered so far, but not most

expensive

The biggest en bloc site ever offered here - Parkview Condominium at West

Coast Park - will be launched tomorrow. And the price? An estimated

$200 million for 407,387 sq ft of land.

The 956-year leasehold site - with effect from May 27, 1928 - is the

largest collective-sale plot marketed in Singapore. But it's not the most

expensive.

Cairnhill Court and a neighbouring bungalow, sold to Li Ka-Shing's

Property Enterprises Development for $370 million in early 2000, holds the

en bloc price record.

The 76 owners of Cairnhill Court pocketed some $3 million to $7.7 million

from the sale, according to earlier media reports.

Parkview's 178 owners will get an average of $1.12 million if the sale

goes through.

Knight Frank, which closed the mega Cairnhill deal, is the marketing

agent for Parkview, which is for sale via a tender that closes on Jan 8,

2003.

At $200 million, the land cost would work out to about $340 per sq ft of

potential gross floor area, including a development charge of some $22.5

million.

The site can yield some 480 condo units of a size averaging 1,200 sq ft.

Breakeven cost is estimated at around $600 psf.

City Developments paid $122 million or $333 psf per plot ratio for Tat

Lee Court in March 2000. CityDev is building the 280-unit Monterey Park

condo there.

Far East Organization's 99-year leasehold condo Blue Horizon at West

Coast Crescent is selling for about $550-600 psf.

Parkview is the sixth en bloc site to be offered this year.

Under the 1998 Master Plan, the site can be built up to 1.6 times its

land area and with a building height of up to 12 storeys.

This is the second collective-sale attempt for Parkview.

In 2000, some owners tried to put the condo on the en bloc market but

failed because they could not garner enough signatures to cross the minimum

80 per cent threshold.

This time around, owners owning more than 80 per cent in share values

have consented to the sale.

'Although there are freehold and 999-year leasehold sites in suburban

areas for sale, none of them are quite as large as the subject site whose

size allows for many development possibilities,' said Knight Frank's

director Amy Khor.

'This site should appeal to developers looking to capitalise on the

opportunity to acquire a site in a pleasant residential enclave.'

- By Andrea Tan Business

Times

27 Nov 2002

|