Grosvenor

Group Ltd, the real estate firm owned by the family trust of

Britain's Duke of Westminster, plans to raise 40 billion yen

(S$622.3 million) for a fund to invest in Japanese properties as the

market recovers.

Grosvenor,

with about US$17 billion in assets, plans to invest in office

buildings and apartments in the greater Tokyo area, said Ken

Nakajima, Tokyo-based managing director at Grosvenor Fund Management

Japan Ltd. The new fund will finance about half of the assets with

loans, a ratio that will allow it to buy as much as 100 billion yen

of properties, he said.

Investors

have started to look at Japan again as a recovery is emerging in the

real estate market. Tokyo was ranked the first in real estate

transactions in the past 12 months with US$28 billion, followed by

Shanghai and Singapore, according to data compiled from New

York-based Real Capital Analytics Inc.

'Investors

have started to show interests,' said Mr Nakajima. 'Japan remains

attractive with its stability among its Asian counter parts.'

Shanghai,

the financial centre of China where January home prices fell for

four straight months, said last week that it's maintaining the

city's housing curbs. Singapore, where fourth-quarter housing values

posted the smallest gain in 21/2 years, introduced new taxes in

December aimed at foreign buyers.

In

Japan, the number of sites where land values were unchanged or

increased in the last three months outnumbered spots that fell for

the first time in 31/2 years, helped by recovering demand around the

Tokyo Bay area, according to a land ministry survey on 150 locations

released this month.

Mr

Nakajima declined to elaborate on how much return the fund will

generate as that has not been finalised. London-based

Grosvenor plans to start buying properties as early as September for

the fund, which will have an investment period of five to seven

years, he said.

The

Duke of Westminster, whose name is Gerald Grosvenor, has a net worth

of US$13 billion, according to Forbes magazine.-- 2012 February 28

Bloomberg

Mitsubishi

increases Tokyo Real Estate investment

Japan's

Mitsubishi Estate said yesterday that it plans to sharply increase new

investments in central Tokyo outside its core district of Maruouchi to

about 100 billion yen (S$1.67 billion) over three years as it sees an

improvement in the market.

The

plans are a rare upbeat sign for Japan's property market and

underscore the better position of developers such as Mitsubishi

Estate which, unlike overseas investment funds, can afford to wait

until new buildings begin generating cash flow.

'It's a good time to buy properties for developing office buildings

now because prices have come down to a reasonable level, and at the

same time we are seeing signs that demand for new buildings will

increase in a few years,' executive vice-president Hiroyoshi Ito

said.

Mitsubishi Estate is one of the most active players in Japan's still

stagnant property market, where no major transactions have been seen

since March when Mitsubishi Estate bought an office building complex

from US investment fund Lone Star for about 90 billion yen.

The developer also announced yesterday the sale of a 30-story office

building in Tokyo for 60.8 billion yen to real estate trust Japan

Real Estate Management.

Mitsubishi Estate plans to spend as much as 30 billion yen a year to

buy land for development, while in 2009 and 2010, when the property

market plummeted in the wake of the global financial crisis, the

developer did not spend more than 10 billion yen each year on new

land, Mr Ito said.

This year it targets spending of 25 billion yen for new land and has

already achieved 80 per cent of the target, he said.

'From this year we are gearing up for new investments,' he said.

Tenants increasingly require safer buildings after the March 11

earthquake that devastated coastal areas of north-east Japan, and

that will help increase demand for new buildings, Mr Ito said.

Mitsubishi Estate is in a good position to buy properties now

because some companies are tempted to sell older office buildings to

seek new and safer buildings, Mr Ito said.

It is still hard to buy properties that went under control of

lenders for good prices because there is still a gap between sellers

and buyers, he said.

'Lenders are also expecting the market to improve in the future so

they want to wait to sell properties until then.'

In the Marunouchi district, where it dominates office development,

Mitsubishi Estate says that it plans to spend 300 billion yen over

the three years, the same pace as in previous years.

Mr Ito's focus is on properties in the areas surrounding Marunouchi

such as Tokyo's Chiyoda, Minato and Chuo wards. --

2011 November 15 REUTERS

Demand for

offices, houses likely to increase as interest rates are kept low

Investors should buy shares in

Japanese real estate companies because demand for offices and houses

is likely to increase as the central bank keeps borrowing costs near

zero, said Bank of America Corp's Merrill Lynch & Co.

Bottoming

out: The number of condos offered for sale in the Tokyo

area rose 27.8% in July while office vacancy fell for the

first time since January 2008

Tokyo's office vacancy rate has

fallen for the first time in 21/2 years, demand for housing is

rising and a decline in land values has slowed, making real-estate

more attractive, Merrill Lynch strategist Masatoshi Kikuchi said.

The Bank of Japan, which kept borrowing costs unchanged on Tuesday,

should also help to spur a recovery in real estate, he said.

'We can see now that the decline

in demand for real estate has pretty much bottomed out,' Mr Kikuchi

said. 'Also, because Japan's interest rates will remain low, we

should see a recovery and investors should start buying these

shares.'

The Bank of Japan kept the

benchmark overnight rate at 0.1 per cent, where it has been since

December 2008. The Topix Real Estate Index, measuring 44

property-related stocks, has risen 12 per cent from this year's low

on July 22, compared with the broader Topix's 0.5 per cent decline

during the same period.

Tokyo's office vacancy rate fell

in July for the first time since January 2008, according to an Aug 5

report by Miki Shoji, a privately held office broker. The number of

condominiums offered for sale in Tokyo and surrounding areas rose

27.8 per cent in July from a year earlier, the Real Estate Economic

Research Institute said on Aug 16.

Japan's land values also declined

at fewer sites for a third straight quarter as property companies

started to purchase land amid a recovery in housing demand, the

Ministry of Land, Infrastructure, Transport and Tourism reported Aug

24.

Mr Kikuchi said that Japan's

stock market should recover further next year, with the Topix index

rising to between 9,000 and 12,000 from January to March as the

global economy strengthens. The Topix closed at 820.99 yesterday.

While foreign investors now view

Japan's equities as a minor part of their global portfolios, Japan

should be able to capitalise on Asia's emerging growth and increase

interest in Japanese companies, he said.

Mr Kikuchi spoke at an investment

seminar attended by more than 1,700 people, including 300 foreign

investors. The number of foreigners at the annual conference jumped

from 279 last year, an increase that shows overseas interest in

Japanese equities has risen, Mr Kikuchi said.

Mr Kikuchi was rated Japan's top

strategist in rankings by the Institutional Investor magazine's 2010

survey and came second in the Nikkei Veritas newspaper's Japanese

strategist rankings this year, according to Merrill Lynch.

At a seminar on Jan 13, Mr

Kikuchi said the Nikkei 225 Stock Average would rise to 13,000 from

10,735.03 by about May as a weaker yen bolstered company earnings.

The gauge climbed 5.6 per cent to this year's high of 11,339.3 on

April 5, and then plunged 12 per cent in May.

Mr Kikuchi also said the Nikkei

225 may rise 12 per cent to 8,500 by the end of March 2009 in a note

to clients on Feb 27 last year. The gauge closed at 8,636.33 on Mar

26, 2009, and rose 7.2 per cent that month. -

2010 Sept 9 Bloomberg

Managers across Japan were

stunned last month when a factory belonging to Ogihara, a Japanese

diemaker, was sold to BYD, a Chinese carmaker that boasts Warren

Buffett as an investor. In a sign of the sensitivity of the matter,

the Japanese firm tried to keep the transaction quiet, never issuing

a press release and refusing all interview requests.

Japan has a long history of

resisting foreigners who seek to buy their way into the country. But

most recent squabbles have at least been with firms from America, a

political ally. Deals involving firms from the Chinese mainland are

touchier because of the two countries’ uneasy relations. This has

kept the number of Sino-Japanese mergers and acquisitions low, even

as China surpassed America in 2007 to become Japan’s largest

trading partner.

Yet the volume of deals is now increasing. The number of

purchases of Japanese firms by Chinese ones almost doubled last year

and their value nearly quadrupled, albeit from low bases (see

chart). The deals usually involve small firms with specialist

technology, which sell a stake or a subsidiary rather than the whole

company, typically for a few million dollars.

Chinese firms are not attracted by Japan’s stagnant domestic

market, with its declining population and chronic overcapacity; they

want to acquire technologies, skills and brands that can be brought

back to China or used in other countries, says Heang Chhor, the head

of the Tokyo office of McKinsey, a consultancy. In return, the

Japanese firm may get not only capital and new management ideas, but

also better access to the burgeoning Chinese market.

This is the case with Laox, an atrophying electronics retailer in

which a Chinese franchisee and Suning, a big Chinese appliance

retailer, recently bought a 51% stake. The new owners have revamped

the firm’s Japanese stores to cater to Chinese tourists who flock

to Tokyo to shop, and plan to open 110 Laox outlets in China over

the next three years. By that time they expect sales in China to

surpass those in Japan.

Importantly, the Chinese owners want to learn from Laox. They

want to improve their relations with suppliers and bring Japan’s

famed standards of service to China, says Luo Yiwen, Laox’s new

boss, a Chinese national who has lived in Japan for two decades.

Before the acquisition Laox’s share price had fallen as low as Ą10

($0.11); it now trades at around Ą110.

Many Japanese are uneasy working for Chinese (much as Americans

disliked working for Japanese carmakers in the 1980s). When Honma, a

high-end golf-club maker, was acquired by China’s Marlion Holdings

in March, the staff were “very shocked”, admits one employee.

But the firm, whose clubs are handmade and individually numbered,

had recently been in bankruptcy. “So we’re just happy to have

jobs,” he adds. Honma’s sales are expected to boom as the new

owner tempts China’s newly-rich golfers with its posh clubs. But

the Japanese employee suspects that recruiting new workers at its

factory in Sakata will be a problem: people would rather work for a

completely Japanese firm.

In some cases, differences in business culture make the tie-ups

unstable. In 2003 companies from China and Taiwan, along with a

Japanese partner, paid Ą1.2 billion for a struggling producer of

colour filters for LCD panels. But the new company, Japan Optical

Display Technology, was shuttered after four years because of

clashes. The Chinese owners were reluctant to pay for environmental

compliance. Moreover, they tolerated manufacturing defects that the

Japanese partner was unwilling to ignore, explains Osamu Mizoguchi,

the former boss. “The philosophies on quality were too

different,” he says.

Despite the difficulties, investors assume such deals will

continue to proliferate. The expected appreciation of the yuan will

fuel foreign deals by making them relatively cheaper (just as a

strong yen did in Japan’s heyday in the 1980s). The fear of being

bought, in turn, may be galvanising Japanese firms. Japanese

businessmen are familiar with the concept of gaiatsu, or

“foreign pressure” to change. But these days the pressure is

coming as much from Chinese firms as from the Western ones to which

the phrase has most commonly been applied.

- 2010 May THE

ECONOMIST

Tokyo's office bargains entice Australian

institution

Australia's largest

institutions have joined other global investors in hunting for

bargains in the world's largest office market, Tokyo

The head of the capital market and

institutional property division of CB Richard Ellis Asia, said

potential Australian investors included the Future Fund, QIC and AMP

Capital Investors.

He said the first major

transaction of a prime Tokyo office block since the onset of the

global financial crisis was last month when Shinsei bank sold

Pacific Century Tower in central Tokyo for $US1.5 billion.

Mr Mackay said daVinci Holdings

had bought the building from Richard Li -- son of the Hong Kong

tycoon Li Ka-shing -- in 2006 for $US2bn.

He said AMP Capital could be the

first to make an acquisition, possibly as

early as the middle of this year.

"Its office in Tokyo has

been researching the office and retail property markets for some

time," he said.

AMP Capital set up an office in

Japan in 2007 and its managing director, Stephen Dunne, said last

month that its focus was on Japan, China and Singapore.

Mr Mackay said the Future Fund

and QIC were more "low key" in their due diligence of the

market.

QIC had $1bn of equity earmarked

for new investment locally and offshore.

He said Japan was the main real

estate investment target for global investors from 2005 to

2007, when four property trusts owning Japanese real estate were

listed in quick succession on the ASX.

Collectively, they owned property

worth $5.6bn at the end of 2008.

He said the new crop of

institutional investors would not be highly geared and would seek

quality rather than high yields.

"The cycle has turned and

the days of Japan-centric listed property trusts are over," he

said.

Mr Mackay said $1.5-2bn worth of

assets belonging to Australian-listed

Japanese real estate trusts was on the market, but most were

"B-grade" buildings and difficult to

sell.

Rubicon Japan Trust, which had

assets of $1.2bn at its peak, is being wound up by its administrator

after its parent, the Allco Group, collapsed.

Galileo Japan Trust secured an

investor in Forum Partners, which injected Y=11bn into the trust to

reduce Shinsei bank's exposure to Y=43.5bn

late last year.

Galileo will begin a selldown over the next three years.

-

2010 January 17 AUSTRALIAN

LVMH Cancels New Tokyo Store

Luxury-Goods Sales

Are Sinking in Japan as New Markets Are Also Pressured

VMH Moët Hennessy Louis Vuitton SA, the world's largest

luxury-goods company, canceled plans to rent a 10-story building in

central Tokyo for a new flagship store, showing how hard the global

economic downturn has hit one of the most important markets for the

luxury-goods industry.

Louis Vuitton's Japan arm informed property developer

Hulic Co. about a month ago that it wouldn't follow through with plans

for a new Tokyo flagship, a Hulic official said Tuesday. The developer

was rebuilding its property in Tokyo's glitzy Ginza district for a

planned store opening in late 2010, but it is now looking for new

tenants, Hulic said.

Officials at Louis Vuitton Japan confirmed that plans were canceled

for the store, which would have been one of the brand's biggest in the

world, but declined to give a reason.

Japan has historically been a major market for luxury goods, and it

has been especially key for Louis Vuitton, which has 56 stores in the

country. Now, as the growth in emerging markets

is showing signs of

strain as well, the falloff in the previously stalwart Japanese market

is especially troubling for luxury-goods companies.

Emerging markets make up about 15% of the luxury-goods sector's

overall sales and had in some places been reporting double-digit

growth. But as the global financial crisis has knocked down Chinese

and Russian stock and property markets, wealthy consumers are under

pressure to cut spending.

Japan, meanwhile, makes up 12% of the luxury sector's global sales

of €175 billion ($240 billion), according to a Bain & Co. study

released last month. But the Bain study said Japan's luxury sales are

expected to decline 7% in 2008, after a 2% decline in 2007. LVMH

reported that in the first nine months of 2008 Japan sales were down

7%, as its world-wide sales grew 4.5% in the period to €11.6

billion.

The deepening recession is just part of LVMH's woes in Japan. There

are increasing signs that young Japanese women are finally tiring of

the luxury brands that previous generations snapped up.

"If it looks good, I don't care what the label is," says

Izumi Sugano, a 21-year-old shop assistant in central Tokyo. A few

years ago in high school, she coveted any bag with a Louis Vuitton

monogram. "Now that I'm working, I realize it's silly to spend so

much on a single bag," says Ms. Sugano, who recently sported a

no-brand bag that cost her less than $100.

That's a sea change for Japan, where women have flocked to buy

brands like Louis Vuitton since it entered the Japanese market in

1978. Luxury labels have tapped Japan's big middle class, and Louis

Vuitton has long counted on Japan as one of its most profitable

markets.

Japan is still Louis Vuitton's No. 1 profit contributor, according

to Melanie Flouquet, an analyst at J.P. Morgan. But Japan's share of

overall LVMH sales, which also include smaller luxury brands like Marc

Jacobs and Fendi, has fallen in recent years to 10% in 2007 from 40%

in 2001, as emerging markets like China and India showed strong

growth.

"Younger Japanese prefer to be stylish and follow trends, but

not spend too much money," says Andrea Fenaroli, Japan president

of Furla of Italy, part of the Furla SpA Group, an Italian midrange

handbag maker.

Since 2000, as Japan's birth rate falls and its population ages,

there are 2 million fewer women in their twenties, the most

fashion-conscious age group.

And an increasing number of women view luxury brands with

indifference, marketers say. A recent survey by the Nikkei Marketing

Journal, a trade publication, shows the percentage of women in their

twenties who own at least one luxury-label bag falling from 57% in

2000 to 44% in 2008.

Some brands have cut prices. Bally and Salvatore Ferragamo have

offered discounts of 25%-30% on their goods sold in Japan since

earlier this year. Furla, which makes 20% of its revenue in Japan, is

selling more bags that use nylon and less expensive parts.

In November, Louis Vuitton lowered prices on nearly all its

products by an average of 7%. Last year, it introduced cheaper lines

like its "Neverfull" handbags, with have no inner lining and

sell for as low as 70,000 yen ($772). That line, first released in

Japan, has become a best seller among women here. -

2008 December 17 WALL

ST. JOURNAL

Lehman Assets in Japan Go on Sale

Bidding started on Lehman Brothers Holdings Inc.'s real-estate

assets in Japan in the past week as creditors in the U.S., Asia and

Japan try to claw their money back from the bankrupt Wall Street firm,

people familiar with the matter said on Friday.

When Lehman went into a tailspin last year, its units around the

world were sold or filed for bankruptcy protection. Lehman Brothers

Japan Inc. filed at the Tokyo District Court on Sept. 16.

Two of the Japanese firm's real-estate loan units, Lehman Brothers

Commercial Mortgage KK and Sunrise Finance Co., sought protection on

the same day. Their liabilities totaled 748.4 billion yen ($8.44

billion).

Japanese brokerage firm Nomura Holdings Inc. acquired Lehman's

operations in Asia, Europe and the Middle East but didn't take any

debt held by the failed U.S. bank.

The timing of the auction is contentious. With real-estate prices

plunging in Japan, mortgage loans are hard to value. Few potential

buyers can borrow capital to make big purchases since banks have

tightened lending criteria.

The administrators outside of Japan, KPMG and Alvarez & Marsal,

believe they would be able to raise more cash at a later date for the

Asian and U.S. creditors they are helping recover capital, according

to people familiar with the situation.

UBS

AG, which is seeking repayment for Japanese creditors to the two

units, however, is pushing for an earlier sale, these people said.

First-round bids for the assets of these two real-estate units were

placed on Tuesday. Companies showing interest include funds at Lone

Star, Cerberus Capital Management LP, Goldman Sachs Group Inc.'s Goldman Sachs Japan Co., Blackstone Group LP

and a Nomura Holdings unit, the people said. - 2009

January 26 WALL

ST JOURNAL

Property failures, price falls

seen for Japan

More bankruptcies, a deluge of

distressed assets and a price slide are in store for Japan's ailing

property industry, as banks recoil from the cheap loans that had

fuelled a boom.

That was the grim assessment by

investors at a conference session in Hong Kong this week, whose title

drawn up a few months ago -- "Japan: a safe haven from the credit

crunch?" -- betrayed the speed of the market's deterioration.

More than 3,000 builders and 425

property firms have failed this year with a combined debt of $25

billion, according to Tokyo Shoko Research. Notable recent victims,

include developer Urban Corp and apartment builder C's Create Co.

And more pain lies ahead.

"A big negative spiral is

coming," said Fred Uruma, chief executive of Touchstone Capital

Securities, which specialises in property finance.

Total lending for property would

probably fall to $8 billion this year from roughly $50 billion last

year, Urama said, putting small and mid-sized developers and

contractors in peril.

Banks, nudged by regulators in late

2007 to cut exposure to the industry, are mostly lending only to big

firms, and cutting loan levels to 55-60 percent of a property's value,

from as much as 80-90 percent a couple of years ago.

Among the major casualties are

asset managers, who grew up with the seven-year-old market in real

estate investment trusts (REIT), securities that are supposed to be

stable because they pay most of their rent to investors as dividends.

Firms such as Kennedix, K.K.

DaVinci Advisors , Pacific Management and Creed typically

built or bought office blocks from developers, filled them with

tenants and sold them on to REITs, which they often managed.

But as debt dried up, the whole

model fell apart.

"LOUSY" ASSETS

Fund manager Re-Plus Inc, which

sponsored Re-Plus Residential Investment 8986.T, set the trend by

filing for bankruptcy protection in September.

Since then, Japan has seen its

first REIT failure -- apartment landlord New City Residence Investment

Corp 8965.T.

More REITs, property firms and fund

managers are likely to hit the wall, which will spark a sale of assets

and a further fall in prices of second- and third-grade buildings,

said Satoru Yamashita, vice president of investment at Mitsui Fudosan

Investment Advisors.

Because of a fall in values,

top-notch Tokyo offices have seen their rental yields rise to around 4

percent, from 2.5 percent a couple of years ago, while yields on

lower-grade buildings have widened to 5.5-6.0 percent from 4 percent.

"Some people are saying they

will go back to where they started a few years ago, around 8

percent," Yamashita said of yields on second grade offices.

"There is still a lack of

really good office buildings in Tokyo," he added. "But the

companies facing difficulties don't own many prime assets."

Although foreign investors are

sniffing around for bargains, the shortage of debt financing means

only those willing to put down a lot of equity are snaring deals.

They include German open-ended

funds that eschew borrowing, such as grundbesitz global, which bought

a Tokyo office block in June, and Union Investment Real Estate, which

plans to spend up to 4 billion euros in Asia over five years.

With Tokyo's REIT index losing 67

percent since a peak in May last year, property trusts should be prime

acquisition targets for funds looking to take them private.

But Seth Sulkin, chief executive of

retail property investor Pacifica Malls, said many assets owned by

REITs were "lousy".

"I looked at one retail REIT,

and even if we got it free it wouldn't make sense," Sulkin said.

"With debt at 60 percent of book value, realistically I couldn't

sell the properties fast enough even at a 40 percent discount."

If the distress continues, the

government could well lean on the country's biggest property firms,

such as Mitsui Fudosan and Mitsubishi Estate, to bail out struggling

property firms, or at least buy assets.

Orix Corp came to the rescue

of struggling developer Joint Corp, injecting 10 billion yen into the

firm in early September, and is also expected to help condominium

builder Daikyo Inc, in which it is a major shareholder.

"Japan is a socialist

country," said Touchstone Capital's Uruma. "If the

government sees too many bankruptcies, they will force mergers. Large

firms like Mitsui (Fudosan) will get the bad end of the stick."

($1=97.89 Yen) -

2008 November 6 REUTERS

Gloomy days:

The capital value of grade A office buildings in Tokyo's commercial

business districts fell 2% on average as of March from three months

earlier, according to an estimate by Jones Lang LaSalle 2008

October 28 BLOOMBERG

To

some Western analysts, it is beginning to look a lot like 1989. In

recent days, Japan's once formidable megabanks and financial titans

are returning to the world financial stage after an absence of almost

two decades, buying pieces of Wall Street institutions, according to The

New York Times.

DEALS

The

US$1.5 billion sale of Resona Maruha Building in Tokyo was the biggest

transaction in the Asia-Pacific in Q2 2008, followed by the US$1.1

billion sale of Shinsei Bank Building (BR), also in Tokyo.

2008 August 19 BUSINESS

TIMES

European

property fund makes first buy in Japan Aberdeen

Property Investors' Degi unit has made its first investment in Japan.

The open-ended property fund has signed the sales contract for La

Porte Shinsaibashi, a fully let retail buiding in Osaka's Shinsaibashi

quarter purchased for €90 million.

- September

4, 2008 Europe

Real Estate

For

the retail business, the key to the Japanese boom, at least

socialogically, is the parasaito shinguro, or "parasite

singles" - an estimated 10 million (mostly women) between the

ages of 25 and 34 who live with their parents and spend up to 10

percent of their annual salary on fashion items. -2008 Spring FQ MAGAZINE

Japanese

Developers' Problems

Threaten to Create Vicious Cycle

Japan has seen a raft

of property developers go to the wall this year as banks have refused

to refinance their loans. Analysts say the bankruptcy filings are

likely to set off a vicious cycle that will weigh on the sector's

shares in the coming months.

The reason:

Real-estate firms that have run into financial difficulty are selling

off assets at fire-sale prices, which will put the value of properties

under strain.

So far this year,

8,916 companies have filed for bankruptcy in Japan, a third of which

were in construction or real estate, according to data compiler Tokyo

Shoko Research Ltd. Big blowups include real-estate management firm

Reicof and condominium developer Suruga. Just last week, Urban

Corp., a Hiroshima-based condominium developer and sales agent, filed

for bankruptcy.

Banks are likely to

clamp down even harder on lending to property firms, and loans granted

are likely to be on more onerous terms, potentially resulting in more

bankruptcies. Recent earnings reports from Japanese banks have shown a

sharp increase in bad debts amid an economic downturn.

"We fear a chain

reaction of bankruptcies," said investment bank Goldman Sachs in

a report to investors. Goldman has a "cautious" stance on

the Japanese real-estate sector, which means the outlook is

unfavorable. The benchmark Topix real-estate index has fallen by about

half since June last year.

Problems started

earlier this year when foreign investment banks, such as Morgan

Stanley, Bear Stearns and Lehman Brothers, cut back on financing

real-estate deals in hopes of reducing risk globally. As a result,

Japan's fledgling commercial-mortgage-backed securities market has

virtually ground to a halt.

The foreign banks

financed some of the most aggressively priced deals by real-estate

funds in Japan. In some cases, they lent up to 90% of the value of

properties for sale in 2007.

Japanese banks are

unlikely to pick up the slack. Their lending to the real-estate sector

has already hit 14% of their loan book, which is higher than what it

was during the Japanese real-estate bubble between 1986 and 1991,

according to analysts at Credit Suisse. This is partly because

companies in other sectors of the economy have been paying down debt

and hoarding cash, and not borrowing so much from banks.

Real estate and

construction, which employ about a tenth of the work force in Japan,

have a big impact on the Japanese sense of economic well being. When

the country's real-estate bubble burst in the early 1990s, it ushered

in an economic slump lasting more than a decade.

Although the Japanese

property market isn't imploding, a recent dip in real-estate

indicators has sparked a rash of fretful domestic newspaper headlines.

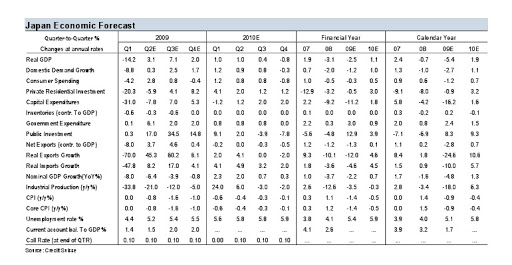

Credit Suisse expects office vacancy rates to rise to 5% in December

from around 3% now. While that level is still low, the rise is likely

to push real-estate shares lower. Credit Suisse rates Japan's

real-estate sector "underperform," meaning it is likely to

yield investors 10%-15% less than the benchmark over a year.

One area that is

unmistakably in free fall is condominiums. The number of condos put on

sale in Tokyo during July plunged 44.5% from a year earlier, and only

half the condos put on the market were sold, according to the Real

Estate Economic Institute Co., well below the 70% rate that condo

makers need to turn a profit.

Analysts say that in

the long run, investors may be able to unearth bargains in Japan's

real-estate sector. Because Japanese real-estate prices didn't rise as

much as in Europe and the U.S., analysts expect Japan to have a

shorter correction. Japanese interest rates remain low, so the yield

on properties is still relatively enticing.

They also believe

that the three major developers, Mitsubishi Estate, Mitsui Fudosan and

Sumitomo Realty & Development, which have strong relationships

with lender banks, will weather the storm better than most.

- 2008 August 21 WALL

ST. JOURNAL

Japanese

Downturn Appears

Likely to Be Shallow but Lengthy

Just how bad will

Japan's economic downturn be? Economists say it likely won't be too

sharp -- but might carry on for a while.

Japan posted its

worst quarterly report on gross domestic product in seven years last

week: The world's second-largest economy contracted at an annualized

rate of 2.4%. A look at the causes shows no single, large problem

hammering down, but a number of factors coinciding to push the economy

into contraction. This, economists say, means Japan likely won't be

battered as hard as it was during its most recent previous downturn,

but it could take a long time to recover.

The current quarter

and the October-December quarter will see just 0.1% expansion over the

previous quarters, forecasts Kiichi Murashima, an economist at Nikko

Citigroup. If Mr. Murashima's prediction turns out to be right, Japan

won't meet the common criterion for a recession of two straight

quarters of economic contraction. But it would put it on course for

anemic growth in 2008. Mr. Murashima predicts expansion of just 0.8%

this year, followed by 0.6% in 2009.

"The recovery

won't come until the second half of 2009," he says. The

stagnation "will likely be protracted."

A long, moderate

slowdown would mean no quick, V-shaped recovery to boost stock prices.

Tokyo's Nikkei Stock Average of 225 companies has fallen 15% so far

this year, and analysts hold out little hope for improvement soon. The

index climbed 0.5% Friday to 13019.41.

It also would mean

Japan's super-low interest rates continue for even longer than

expected. After abolishing an emergency target of zero for short-term

rates in 2006, the Bank of Japan last raised its target in February

2007 -- to just 0.5%. Some economists now think it won't raise the

rate until 2010, meaning limited increases in long-term borrowing

rates and less support for the yen. The bank is expected to leave its

rate target steady at a two-day policy-board meeting that ends

Tuesday, but it might downgrade its assessment of the economy.

Politically, a long,

shallow downturn could damage Prime Minister Yasuo Fukuda's prospects

of winning the next general election, which must be held by September

2009. His cabinet has an approval rating in the 20%-to-30% range,

according to some opinion polls, raising the likelihood of a victory

by the opposition Democratic Party of Japan. The DPJ has never held

power, and its recent policy statements suggest a return to public

spending to aid weak regional economies.

To counter this DPJ

message, Mr. Fukuda's Liberal Democratic Party might push for more

public funds for the provinces. Taro Aso, the LDP's new

secretary-general, has been quoted in the past two weeks as calling

for greater public spending. He also said the government would likely

miss a target of 2011 for achieving a primary budget balance (revenue

minus spending, not including the cost of debt servicing).

Meanwhile, Mr. Fukuda

appears to have abandoned the quest of former Prime Minister Junichiro

Koizumi to promote structural changes to spark economic activity.

"There is no

concept [in the current administration] of raising potential growth

through deregulation," says Ryutaro Kono, an economist at BNP

Paribas. He thinks Japan's education, medical and farm sectors could

be enlivened through exposure to greater competition. But government

officials and other "LDP supporters are concerned not to lose

their vested interests through deregulation."

Japan's fundamentals

aren't that bad: Unemployment and inflation are low, and banks have

been relatively unscathed by losses related to subprime mortgages.

Corporations on average increased their profits every year from 2002

to 2006.

But Japan has been hit by problems from overseas.

Because Japanese manufacturers import almost all

their raw materials, the rise in world commodity prices has eroded

profits. Annual wholesale inflation -- the rise in the prices

companies have to pay for things like materials -- jumped to a 27-year

high of 7.1% in July. But, in the face of low growth in consumer

spending, the consumer-price index -- which indicates how much

retailers can raise prices -- rose just 2% in June over the previous

year.

The squeeze on corporate profits has crimped

investment in plant and equipment -- traditionally a big driver of

Japanese economic growth. It also has held down wages, discouraging

consumer spending.

But even if commodity prices fall back and companies

learn to cope with higher costs, Japan faces other troubles. Weakness

in the U.S. and Europe as well as a possible post-Olympic slowdown in

China could hurt exports. "External demand, which has been the

driver of the Japanese economy, will likely stagnate further," in

particular between October and March, wrote Morgan Stanley economist

Takehiro Sato in a report last week. He forecasts Japan's economy will

grow 1% this year -- and just 0.6% in 2009.

- 2008 August 18 WALL

ST JOURNAL

Builder

Urban Joins Failures

Of Japan's Real-Estate Sector

Japanese property

developer Urban Corp. filed for court-led rehabilitation Wednesday

when it collapsed with 255.83 billion yen ($2.34 billion) in

liabilities, becoming the nation's biggest corporate failure so far

this year.

The Hiroshima-based

firm, which joins a growing number of casualties in Japan's faltering

real-estate sector, said the Tokyo District Court ordered the

protection of its assets immediately after the filing. Its shares will

be delisted from the first section of the Tokyo Stock Exchange Sept.

14.

Japan's real-estate

sector is buckling from a slowing market stemming from the U.S.

subprime problem. Wary of doling out new loans, financial institutions

are scaling back their lending to the sector, which is spurring a

string of corporate failures.

Last month,

condominium developer Zephyr Co. filed for court protection with debt

of about 95 billion yen, while construction company Suruga Corp. went

under in June with debts valued at 62 billion yen.

Urban, whose business

includes condominium development and investment in nonperforming real

estate, said that the worsening situation has made it impossible to

raise funds via a capital alliance.

"We've given up

the idea of self-resuscitation and have decided to rebuild through

court-led rehabilitation," the company said.

The inability to pay

off loans with due dates in and after mid-August also prompted the

company to file for the court-led rehabilitation. Hiroshima Bank Ltd.

is Urban's main lender with outstanding loans totaling 12.9 billion

yen.

Shares of Urban have

dropped about 80% since late June. In trading in Tokyo on Wednesday,

the issue ended at 62 yen, down one yen, giving it a market

capitalization of 14 billion yen.

Urban has already

agreed to sell 30 billion yen of convertible bonds to an arm of French

bank BNP Paribas SA. Officials from BNP Paribas weren't available for

comment.

An Urban spokesman

said the convertible-bond deal with BNP Paribas still stands.

Urban also said

Wednesday that it reported a net loss of 45.42 billion yen in the

fiscal first quarter compared with a year-earlier profit of 15.92

billion yen. Sales fell 43% to 49.91 billion yen during the April-June

quarter. - 2008

August 14 WALL

ST JOURNAL

Tokyo residential property set

for full-blown decline Japan's slowing economy and the credit crisis has damped commercial,

residential demand

Tokyo residential property prices may be poised for a major decline because

of excess housing supply and flagging demand, said Minoru Mori,

chairman of Japan's biggest privately held developer. 'We foresee

full-blown drops in residential property prices,' Mori Building Co's

chairman said in an Oct 25 interview in Shanghai.

Japan's slowing economy and the credit crisis that tightened

lending has damped demand for commercial and residential property in

Japan. The slump in Tokyo's condominium market may last longer than

the drop after Japan's asset-price bubble burst in 1990, according to

an estimate by the Real Estate Economic Research Institute.

Condo supply in Tokyo fell 24 per cent for the first six months of

the year from the same period a year earlier. The number of new condos

put up for sale in Tokyo, which stayed above 80,000 units since 1999,

fell to 69,194 units in 2007 because sales declined and inventories

rose. Commercial real estate is holding up better than residential

property, said Mr Mori.

'Tokyo's commercial property market remains relatively healthy. The

current price decline probably won't be more than 10 per cent,' Mr

Mori said.

Tokyo-based Mori has scrambled to manage the impact of the global

financial market turmoil. Lehman Brothers Holdings Inc, which last

month filed for the largest bankruptcy in history, was a tenant of the

developer's Roppongi Hills complex, occupying 275,000 square feet of

office space.

Nomura Holdings Inc, which agreed to buy Lehman's European and

Asian assets, has expressed an interest in taking over Lehman's lease

at Roppongi Hills, Mr Mori said in the interview. Japan's biggest

brokerage also 'hinted' at possibly increasing the floor space it

leases at the complex, he said.

Other tenants at the complex such as Goldman Sachs Group Inc are

under long- term agreements that incorporate increases in the rents

they pay, Mr Mori said. 'On a contractual basis, we don't foresee any

problems,' he said.

The capital value of grade A office buildings in Tokyo's commercial

business districts fell 2 per cent on average as of March from three

months earlier, according to an estimate by Jones Lang LaSalle.

As commercial prices declined, Mr Mori said now is the time to

prepare for land acquisition for large-sized projects similar to

Roppongi Hills. 'We have plans to introduce second, third, fourth and

fifth Roppongi Hills,' said Mr Mori. 'This is a good time to plan for

large-size projects.'

Mori is in talks with local residents to redevelop

Toranomon-Roppongi. The developer plans to build a 46-storey

commercial tower and a six-floor residential building on a 15,350

square metre site in 2009.

Other projects under planning include Loop Road No 2 from Toranomon

to Shimbashi in central Tokyo and a waterfront development project in

Yokohama, according to the company's website.

These projects will require infrastructure such as roads and large

blocks of available land, both of which may take some time, he said.

Mori Building's Shanghai World Financial Center, China's tallest

building, was opened to the public on Aug 30. Space in the building

was leased 'faster than expected' to near 50 per cent of capacity

currently from 40 per cent in August, Mr Mori said.

Japanese financial institutions such as Mizuho Financial Group Inc

and Sumitomo Mitsui Financial Group Inc have taken space, he said.

Demand for space may slow with the opening of new office developments

in Shanghai, such as Sun Hung Kai Properties Ltd's Shanghai IFC

complex, located next to Mori's building.

'As new developments come on line, it might be difficult to enjoy

the same occupancy rates as before, and net demand might decline

somewhat,' Mr Mori said. -- 2008 October 28 BLOOMBERG

Japanese condo developer

tightens belt

Japanese condominium developer

Joint Corp plans almost no new investments this year as it focuses on

reducing its assets to ride out an increasingly negative business

environment including an exodus of foreign investment, a company

executive said on Monday.

Shares of Joint and other Japanese

real estate developers have been hit hard in recent sessions amid

concerns about the health of the sector due to the global credit

crunch and weak consumer spending.

Japan's property sector has also

been hurt by tighter bank lending and soaring prices for steel and

other construction materials.

To survive this business

environment and improve its cash situation, Joint is mulling selling

off some of its vacant land, said director and executive officer

Hisahi Oribe.

'We don't want to be seen as having

passive business plans, but our business is currently up against a

really strong headwind,' Mr Oribe told Reuters in an interview.

'For a while, all we can do is

simple things just to improve our business,' he said. The Tokyo-based

midsized developer plans to sell land, buildings and other inventories

to reduce its fixed assets to 150 billion yen (S$1.90 billion) for the

year ending in March 2009 from 230 billion yen as at March this year.

Joint may post special losses this

year for writing down such assets, but the amount will likely be small

as it already wrote down 11 billion yen worth last business year, said

Mr Oribe.

'About 80 per cent of our

condominium-development projects have already been inked or paid,'

said Mr Oribe.

He added that the company would not

have to spend much on new projects during the course of this business

year.

The recent sell-off of Japanese

real estate-related stocks comes as the global credit crisis muddies

the outlook for Japan's once-soaring property market.

Adding fuel to investors' worries

over the sector's financial health, a series of Japanese contractors

and real estate developers including Suruga Corp have fallen into

bankruptcy.

The Tokyo Stock Exchange's Reit

index has dropped about a quarter this year.

Japanese Reits' market value

tumbled to 4 trillion yen in March this year from 6.8 trillion yen in

May last year when it hit its peak.

Mr Oribe said, however, that

although there was a slew of bad news in the sector, the recent

sell-off of Joint shares was 'abnormal and emotional'.

'It is abnormal that even big real

estate players have a PBR (price to book value ratio) of below one,'

he said. 'Our business environment really is tough, but I think

investors have been a bit too emotional,' he added.

Joint shares, which have a PBR of

0.29, fell as low as 440 yen during morning trade yesterday, their

lowest intraday level since August 2003, but bounced back to finish up

5.4 per cent at 509 yen. - 2008

July 8 REUTERS

Property firms raise rents in

central Tokyo

Average rent in five central wards up 12%

last month from June 2007

Japan's leading estate firms including

Mitsui Fudosan Co have begun proposing big rent rises in central

Tokyo, where office vacancy rates have been hovering near 20-year

lows.

hese rock-bottom vacancy rates have

helped Mitsui Fudosan and rival Mitsubishi Estate Co weather tougher

times for much of Japan's property market, which has been hit by

tighter credit and stricter apartment building codes.

Mitsui Fudosan, Japan's largest

real estate developer, said yesterday that it was in talks with

tenants to raise office rents in central Tokyo by an average of 10-15

per cent.

The country's second-largest

developer, Mitsubishi Estate, also said that it was in talks with

tenants to raise office rents in the Marunouchi area of central Tokyo

by 15-20 per cent.

Another major developer, unlisted

Mori Trust Co, said that it was preparing to raise office rents in

central Tokyo's Minato district by an average of 20 per cent.

The office vacancy rate in Tokyo's

23 wards stood at 2.1 per cent last month - the lowest since the

bursting of Japan's asset-inflated bubble economy in 1990, according

to Ikoma Data Service System, a research firm specialising in the

market for office buildings.

Average rent in Tokyo's five

central wards last month was 15,120 yen (S$199) per approximately 3.3

sq m. That marks a 12 per cent increase from 13,530 yen in June of

last year, according to the most recently available data from Ikoma.

'Tokyo's office market is extremely

tight,' said Ikoma researcher Mitsuhiro Asada.

'With signs of an economic

recovery, many companies started hiring more people, and that's making

them want to move to bigger offices,' he said.

He added that such conditions would

likely last for a while, helping real estate firms' businesses.

Mitsubishi Estate said that it was

seeking the rent increase given the tight office market situation in

the Marunouchi area. It said that its vacancy rate in that district

was just 0.19 per cent as at the end of March, the lowest since it

started disclosing the data in 2003.

- 2008 May 25 REUTERS

Citi Japan sells head office to

Morgan Stanley The sale and lease-back deal will increase balance sheet efficiency and

mitigate property risk, says Citi

Foreign banks keen to raise cash could

increasingly turn to Japan, say analysts, thanks to its liquidity.

While the commercial real estate markets in the UK and the US are

frozen, Japan has become one of the few major markets where deals can

take place, notes Yoji Otani, a real estate analyst at Credit Suisse

in Tokyo.

That’s the logic which has pushed Citi

Japan to offload its Citibank Centre head office (the land and the

building) to Morgan Stanley. Details of the transaction were not

disclosed by either party, but according to the Nikkei Business

Daily, the acquisition price was $445 million. Neither side would

comment - but the cash will be welcome as a contribution to Citi's

balance sheet, hurt by subprime losses.

The building is in Shinagawa, a prime real estate area where the

headquarters of Sony, Mitsubishi and Canon are also located. The

building houses Citi Japan’s retail and corporate banking divisions.

Aside from the head office, Citi has 25 branches and nine sub-branches

in Japan. The US bank will lease the building back from Morgan

Stanley.

According to the Japan Real Estate

Institute, real estate prices in the six largest Japanese cities have

emerged from a trough of 67 points on the index in 2004 to 96 in

September 2007. The index was at 500 points in 1990, the peak of

Japan’s economic bubble. Citibank Centre was built in 1992.

Based on the Nikkei data, the price paid represents a yield of

3.5%-4%, estimates Otani. “It’s not a very exciting yield, it’s

very much average for the market,” he comments.

The Morgan Stanley fund (Morgan Stanley Real Estate Investment) that

bought the building is not a high-risk, high-return fund, but tends to

invest in low-yielding, stable investments, making the yield

appropriate. “The deal was done at fair value,” says Otani.

The fact that the fund is based in Germany could be a reflection of

the difficult state of the European real estate market, say observers.

European funds could have large amounts of money on their books which

they need to spend, even if the projects are far away in Asia.

- 2008 February 20 FINANCE

ASIA

A securitisation expert who preferred to speak off the record, says

that the market for commercial mortgage-backed securities (CMBS) is

pretty robust in Japan, and that investors are not requiring the

"irrational yields" being demanded in Western markets. A

functioning securitisation market is an important precondition for a

rising real estate market.

“The evidence is that investors have plenty of cash to spend next

fiscal year, and Japanese government bond (JGB) yields keep trending

down. So, once the markets stabilises, I would not be surprised if the

CMBS market performed reasonably this year as investors look to

maximise yields,” he says.

The Tokyo real estate market could see more such deals as

cash-strapped foreign institutions, hammered by the subprime crisis,

seek to strengthen their balance sheets. But Credit Suisse’s Otani

believes that prices will have to fall and yields rise as the Japanese

economy slows and the credit contraction starts to bite.

The broader macro situation is not conducive to optimism on the real

estate market. In the third quarter, the economy grew at 0.9% in real

terms. Exports have increasingly been driving the economy as domestic

consumption weakens on slow wage growth. A weak performance from Japan

ex-Tokyo in the small company sector is a huge concern for the

government.

Citi’s woes represent an opportunity for Morgan Stanley, which has

built a position in real estate over the past decade and has become

one of the biggest hotel operators in Japan. Last year the bank bought

a chain of 13 hotels from All Nippon Airlines for $2.4 billion, which

it manages through its Panorama subsidiary. Panorama often works

closely with existing hotel managers to increase the value of the

hotels ahead of a sale. Morgan Stanley now has 10,000 rooms in Japan,

putting it among the top 10 hotel operators nationwide. Over the past

10 years, Morgan Stanley has invested $20 billion in Japanese real

estate.

Earlier this month, Morgan Stanley offloaded the Westin Tokyo to the

Government of Singapore Investment Corporation for around $770

million. Other notable deals in the past six months include Goldman

Sachs’s acquisition of the Tiffany flagship store for $305 million

in August last year. Somewhat ironically, the Tiffany building in New

York was once owned by Japanese investors, but they sold out after the

bubble burst.

Three Tokyo Waterfront City projects awarded Developments will create more office,

residential space

Mitsui Fudosan Co, Japan's largest

real estate developer, Daiwa House Industry Co and others won three

waterfront projects worth US$1.81 billion to create more office and

residential space in Tokyo.

Mitsui Fudosan, Daiwa House and

Sankei Building Co will spend 79.2 billion yen (S$1 billion),

including the cost of land, to develop an office building, the Tokyo

Metropolitan Government said on its website. Tokyo Tatemono Co, a

111-year-old property firm, won the right to develop an office site at

a cost of 107.6 billion yen.

The plans are part of Tokyo's

Waterfront City project about six km from downtown on 442 ha of

reclaimed land. The city expects to attract 70,000 residents and

42,000 workers to the area. Average waterfront prices are about a

quarter of land prices in nearby Shimbashi, part of central Tokyo,

according to government figures.

'With the office vacancy rate being

very low, some tenants may seek space in that area,' said Masahiro

Mochizuki, a real estate analyst at Credit Suisse in Tokyo. 'However,

I am concerned about the profitability of these projects because the

location is not that great.'

Japan's commercial land prices rose

for the first time in 16 years during the 12 months through June, as

real estate companies and investors sought sites to develop. Demand

for office space in Tokyo pushed rents to a 13-year high.

Shares of Mitsui Fudosan rose 0.2

per cent, or five yen, to 2,515 on the Tokyo Stock Exchange. Tokyo

Tatemono dropped 0.6 per cent to 1,122, and Daiwa House fell 0.9 per

cent to 1,488.

The Mitsui Fudosan site is 32,904

square metres, while Tokyo Tatemono's is 29,640 sq m. The third site

will be used to relocate Musashino Joshi Gakuin, a girl's junior and

senior high school, onto a 13,014 sq m location.

- 2007 December 27 BLOOMBERG

Tokyo to replicate Canary Wharf Japan wants more financial

institutions to open Asia HQ in capital

Yuji Yamamoto, Minister for Japan's

Financial Services Agency, said the country plans to replicate

London's Canary Wharf in an effort to get more financial institutions

to set up their Asia headquarters in central Tokyo.

Japan wants to take measures to

attract more hedge funds, banks and other financial institutions to

the nation's markets. Mr Yamamoto is seeking to ease rules that

separate banks and brokerages while strengthening the authority of the

Securities and Exchange Surveillance Commission.

'We've set strengthening of Japan's

financial markets as a priority in the June paper, which will outline

the basic economic reforms of Prime Minister Shinzo Abe's government,'

Mr Yamamoto said at a conference in Tokyo yesterday. 'We are aiming at

taking a similar type of zoning approach as that seen in Canary

Wharf.'

Mr Yamamoto said the zone targeted

is along the Sumida River, starting from the Nihonbashi district,

taking in the Bank of Japan, and Kabuto-cho, where the Tokyo Stock

Exchange is located. New high-rise buildings are to be built with

24-hours operations 'to enhance services for people who work across

different time-zones and suffer jet-lag,' he said.

Japan needs to make financial

regulation more transparent and create new markets to attract more

hedge funds to win a greater share of global investment, an advisory

panelto the agency said last month. Government committees are having

'positive and bold discussions' to promote reforms, Chief Cabinet

Secretary Yasuhisa Shiozaki said last month.

The Council on Economic and Fiscal

Policy, which draws up reform plans and outlines budgets, said last

month the nation's financial markets for securities and commodities

should be consolidated under the Tokyo Stock Exchange to create a

single trading venue that can compete with global rivals for investors

and products.

However, he said Tokyo has fallen

too far behind other financial centres in its ability to attract

foreign bankers and capital. Japan accounts for just 5 per cent of

financial industry profits worldwide. Only 28 non-Japanese companies

were listed on its stock exchanges in 2005, down from 96 in

1990. High taxes and finicky regulators are often blamed for

driving foreigners to smaller but more cosmopolitan centres such as

Singapore and Hong Kong.

'Japan's internationalisation

efforts have lagged,' Mr Yamamoto said in a speech to the American

Chamber of Commerce in Japan. 'We have to find a way to reverse this

trend.

'That's my challenge.'

As another potential step,

private-sector panel members have proposed merging Japan's commodities

exchanges with the Tokyo Stock Exchange to create a single, all-

encompassing bourse, though ministries that now regulate commodities

trades oppose the move.

On taxes, Mr Yamamoto acknowledged

that low-corporate-tax countries such as Singapore had an easier time

luring foreign firms than Japan - a situation he compared with

Ireland's edge over the UK since Ireland slashed taxes in the 1990s.

Beyond recognising the problem,

however, he gave no hint that Japan planned to ease it tax

rates.

Even if Japan is successful in

making its markets more open, largely monolingual Tokyo may still have

a tough time drawing foreign bankers, according to Kirby Daley, a

strategist at the brokerage Fimat who has lived and worked in both the

Japanese capital and Hong Kong.

'For families coming from Europe or

the US, the cultural and language barriers immediately and continually

have put Tokyo at a disadvantage to Hong Kong and Singapore.'

- Bloomberg,

Reuters 22 May 2007

Tokyo aiming to be Asian financial

hub

It is not so much a case of the

business coming to Tokyo as a financial centre as of Japan going to

where the business is.

Over the past few decades, Tokyo,

Hong Kong and Singapore have vied from time to time to become the

premier financial centre of the region. Singapore has established

itself as a financial bridge between South and South-east Asia while

Hong Kong has retreated to a China-dependent position and Shanghai has

begun to assert its own claims. Tokyo meanwhile has seemed to slip out

of contention, but something is stirring again now.

Japan's recently-appointed

Financial Services Minister Yuji Yamamoto is hatching a scheme to turn

Tokyo into the 'London' of East Asia, so far as financial services go,

while Tokyo Stock Exchange (TSE) president Taizo Nishimuro has managed

to link the TSE with both the London and New York stock exchanges in a

three continent-spanning alliance.

Could this mean that Tokyo is

finally about to become the monarch among Asian financial centres?

Perhaps, but what is more likely to

happen is that Tokyo will once again demonstrate the truth of the

saying that Japan is 'in Asia but not of Asia'. A part of the nation's

colossal savings will be invested in China and India but increasingly

Japanese capital seems likely to flow into Russia and Eastern Europe

as well as to exotic spots like Brazil, and Tokyo could become home to

IPOs and stock exchange listings originating outside Asia.

This is happening already, even

before Mr Yamamoto's plans begin to get off the ground and before Mr

Nishimuro's commendably pragmatic schemes for the TSE begin to bear

fruit.

Very large sums of Japanese debt

and equity capital are being invested in Russia and Eastern Europe,

via syndicated loans, and into London or New York-led IPOs for state

and privately owned entities from these countries, as well as through

investment funds.

It is not so much a case of the

business coming to Tokyo as a financial centre as of Japan going to

where the business is. The conduits are Japanese megabanks such as

SMBC, Mizuho and Mitsubishi UFJ or investment banks and securities

houses such as Daiwa SMBC and Nomura.

These are high value transactions

but because Japanese firms do not enjoy the same glamour as the

Goldman Sachs, UBS' or HSBCs of this world they remain relatively low

profile.

While Japan does not enjoy the same

degree of sophistication in financial techniques as do New York and

London, or Hong Kong and Singapore for that matter, it does have money

-huge amounts of it. A great deal of this money is in the hands of

individual investors and they are happy to place it with banks and

securities firms and send it offshore in search of much higher yields

than it can earn at home.

Japanese investors and authorities

do not even require that foreign entities wanting to raise capital in

Japan should list their securities on the TSE. These investors,

obligingly, are happy to trade securities they receive in return for

their capital on London or New York, despite the marginal

inconvenience of different time zones, and to accept the fact of being

'in foreign parts' in return for what they perceive as the greater

safety and transparency of dealing on the NYSE or the LSE compared to

the TSE.

Not surprisingly, one party that is

not happy is the TSE itself, having seen the number of foreign

companies listed in Tokyo plunge from around 130 at the height of

Japan's bubble economy to just 25 now, and having watched the

exchange's total capitalisation slip from near parity with New York's

to roughly one third of New York's US$13 trillion now.

The TSE's share of global stock

market capitalisation has meanwhile slipped from one third of the

total to only one tenth.

Wisely, Mr Nishimuro has abandoned

the fiction that the TSE can recover former greatness simply by urging

Asian companies from China, India, Asean and beyond to list their

stocks on the Tokyo Exchange, or solely by entering into collaborative

alliances with other stock exchanges in these various countries.

Recognising the technological and

other shortcomings of the TSE still, he has instead cemented working

relations with the NYSE and the LSE where systems and standards are

state of the art. This promises that, in terms of technological and

trading competence at least (no more embarrassing computer system

crashes or trading system errors), Tokyo should be able to emerge

within a couple of years as the primus inter pares among Asian stock

markets - and with a thoroughly modernised, de-mutualised and

publically listed stock exchange that is ahead of others in more

respects than just having the world's second largest capitalisation.

But all this does not add up to

making Tokyo a world class financial centre, or even the best in Asia.

So what does Mr Yamamoto have in

mind? Little detail has been revealed as yet, probably because the

minister has not been long enough in office. However, past schemes

such as launching an offshore banking centre in Tokyo, or even Japan's

much lauded financial sector Big Bang in the 1990s have failed to

overcome fundamental obstacles to Tokyo's ascendancy.

Mr Yamamoto has spoken of creating

a London-style 'Canary Wharf-style' quarter in Tokyo where the

financial community drawn from all parts of the world can work, live

and socialise together.

Laudable, no doubt, but a

financial centre cannot be socially engineered. A much higher degree

of English competency and a basic change in acceptance of foreigners

(gaijin) and foreign practices in Japan are needed as building blocks

in order for Tokyo to become a cosmopolitan financial centre.

Singapore and Hong Kong need not tremble yet. -

by Anthony Rowley SINGAPORE

BUSINESS TIMESTokyo Correspondent 2007 March

1

Japanese real estate prices rise after 14 years

Japanese land prices rose for the first time in 14 years in 2005,

signalling an end to the persistent asset deflation that dragged the

nation's economy into recession in the early nineties.

Data released yesterday by the National Tax Agency also showed

that price gains were spread across Tokyo and four other cities -

Chiba, Aichi, Kyoto and Osaka - underlining the strength of the

recovery and alleviating concerns that it would be limited to a few

patches in the capital. In 2004, Tokyo had been the only prefecture

in which land prices rose. - - By Mariko Sanchanta in Tokyo

FINANCIAL TIMES August 2 2006

Banks fuel property boom

Tokyo's real estate market hums as Japanese

banks, eager to expand their loan portfolios, pour ever more cash into

property. This is no flashback to the country's doomed 1980s asset

bubble: It's happening now.

New lending by Japanese banks to real estate

developers rose 15 percent to 8.18 trillion yen (HK$570.96 billion) in

the business year to March 31, Bank of Japan data show, even as the

volume of new loans for capital investment of all kinds fell by nearly

3 percent.

``It's like a mini-bubble, it's true,'' an

executive at a major Japanese real estate firm said, describing the

exuberance with which Japanese banks have returned to property

finance, lured by bottoming land prices and new demand from commercial

and residential builders.

But there are crucial differences between

banks' real estate lending today and the speculative frenzy of nearly

two decades ago, which left Japan's economy paralyzed and banks

saddled with billions of dollars in soured loans.

``Banks have changed the way they lend, the

way they manage risk,'' said Jason Rogers, chief credit analyst at

Barclays Capital in Tokyo.

A key innovation is the expansion of

non-recourse lending, which limits collateral to a single building or

project, protecting the borrower's other assets and limiting the size

of loans.

Repayment plans rely on rents and other cash

flow, rather than expected land-price rises. Banks are also more

careful to share risks with developers, typically funding 60-65

percent of a project with loans and leaving builders to pay for the

rest through equity.

The rise in property finance reflects banks'

return to health, analysts say. Bad loans at Japan's leading banks

fell to less than 4 percent of total lending last financial year, in

line with their global peers, from more than 8 percent in 2002.

Epitomizing the turnaround is Mitsui Trust Holdings, Japan's

seventh-biggest bank and one of the biggest property lenders with

close to one trillion yen in outstanding real estate loans.

The bank, one of the hardest hit by the

bad-debt crisis, posted an 85 percent rise in annual net profit for

2004/05 and forecast further gains. Growth in real estate lending has

fed a string of new office towers reshaping Tokyo's skyline.

In a sign of renewed demand for property,

commercial land values in Tokyo's five most developed wards rose in

2004 for the first time in 14 years. At the same time, mortgage rates

have fallen, dropping below 2 percent in some cases for a 10-year

loan, enhancing the appeal to residential buyers.

Still, while new non-recourse real estate

loans topped four trillion yen last year, that amounted to just 1.5

percent of Japan's domestic lending, said Yoshinobu Yamada, a bank

analyst at Merrill Lynch.

``Experiences during the bubble era have

given many people the impression that real estate lending equals high

risk,'' he said. But banks' more diverse loan portfolios and other

advances in risk management mean there is little chance of a return to

bubble-style recklessness, he said.

Instead, he and others familiar with the

industry say the biggest risk for banks is that a rising supply of

loans could squeeze margins and erode profitability.

Foreign banks that led the return to

property finance in Japan in the late 1990s enjoyed sizeable lending

premiums, but these have fallen sharply as Japanese banks have joined

the fray.

Premiums on real estate loans compared with

benchmark interbank lending rates have fallen by a third to half since

2000, a property executive said, and in some cases banks are lending

at rates below what the actual lending risk demands. ``With the entry

of the Japanese banks, the spreads really started to get squeezed,''

the executive said. ``They're being squeezed every day.'' REUTERS

15

July 2005

Tokyo properties show

recovery

Prices are rising, and construction

demand is on the upside nationwide

Tokyo average

residential land prices rose in Tokyo's five main wards last year for

the first time since 1987, indicating Japan's slump in property values

may be ending. Commercial real estate prices in those five areas also

gained for the first time in 14 years.

Looking up:

Residential and commercial land prices are beginning to recover

throughout Metropolitan Tokyo, except in Shinjuku. Characterised

as 'accelerating' by market observers, the recovery is expected

to bolster growth.

The average price of residential land in

Chiyoda, Chuo, Minato, Shinjuku and Shibuya wards rose 1.4 per cent in

2004, the Ministry of Land, Infrastructure and Transport said

yesterday in a statement.

Commercial land values also rose, gaining

0.5 per cent in the same region on average.

Signs of an end to land price deflation may

help bolster growth in Japan as property owners gain more confidence

about the future and increase consumption, economists said.

The world's second-largest economy has had

four recessions since land and other asset prices began tumbling at

the end of the 1980s.

'Stable-to-rising land prices are going to

encourage activity in the real-estate, construction, and housing

sectors,' Richard Jerram, chief economist at Macquarie Securities Ltd

in Tokyo, said before the report.

'It's a clear positive for the economy,' he

added.

Nationwide, land prices declined for a 14th

straight year, slipping 5 per cent, the smallest drop since 2000, the

report showed. Property values fell 6.2 per cent in 2003.

Japan's land prices haven't risen since

peaking in 1990. The slump since then has erased about two-thirds of

the value of commercial property purchased in that year and about half

of that for residential real estate.

Annual nationwide construction orders rose

for the first time in four years in 2004, increasing 4.2 per cent to

13.1 trillion yen (S$201 billion), the land ministry said on Jan 31.

Housing starts rose 2.5 per cent last year, a second consecutive

yearly gain.

'Increases in land prices accelerated in

some of Japan's metropolitan areas and the decline in the rest of

Japan has narrowed,' Hiromichi Iwasa, chief executive of Mitsui

Fudosan said.

'These factors reflect a strengthening

Japanese economy,' he added.

Japan emerged from recession at the end of

last year, expanding at a 0.5 per cent annual pace in the three months

ended Dec 31 after shrinking in the two previous quarters.

'We have started to see the trend of falling

land prices in the Tokyo, Osaka and Nagoya areas coming to an end as

the business environment improves,' the ministry said in the report.

Space in Marunouchi Building, a high-rise

office and shopping complex owned by Mitsubishi Estate Co, Japan's

second-largest developer, remains the most expensive in central Tokyo,

at 22 million yen per square metre, up 4.8 per cent from 2003.

Residential and commercial land prices rose

in all the five main Tokyo wards last year except Shinjuku, where they

fell 0.3 per cent and 1.1 per cent, respectively.

A recovery in property prices would probably

help Mizuho Financial Group, Sumitomo Mitsui Financial Group and other

lenders that have accepted real estate as collateral for loans.

Land prices rose an average of 8.7 per cent

a year in the decade through 1990, then collapsed, leaving banks with

loans that weren't being repaid.

Japan's banks cut bad loans by about 11 per

cent to 23.7 trillion yen in the six months to Sept 30, 2004,

according to the Financial Services Agency.

'Falling land prices, financial system

distress and corporate sector restructuring are all tied together,' Mr

Jerram of Macquarie Securities said.

'Rising land prices go hand-in-hand with a

healthy financial system.'

Prices in the Tokyo region - that includes

neighbouring Saitama and Chiba prefectures, the cities of Yokohama,

Kawasaki and other municipalities - fell 3.2 per cent, the least since

the declines started in the area in 1991, according to yesterday's

report.

Japan's residential land prices fell 4.6 per

cent, the slowest decline since 2000, while nationwide commercial land

prices dropped 5.6 per cent, the smallest decline since 1991, the

ministry said.

'The degree of weakness is getting less,'

said Peter Morgan, chief economist at HSBC Securities Japan Ltd. -

Bloomberg